{kind=link}

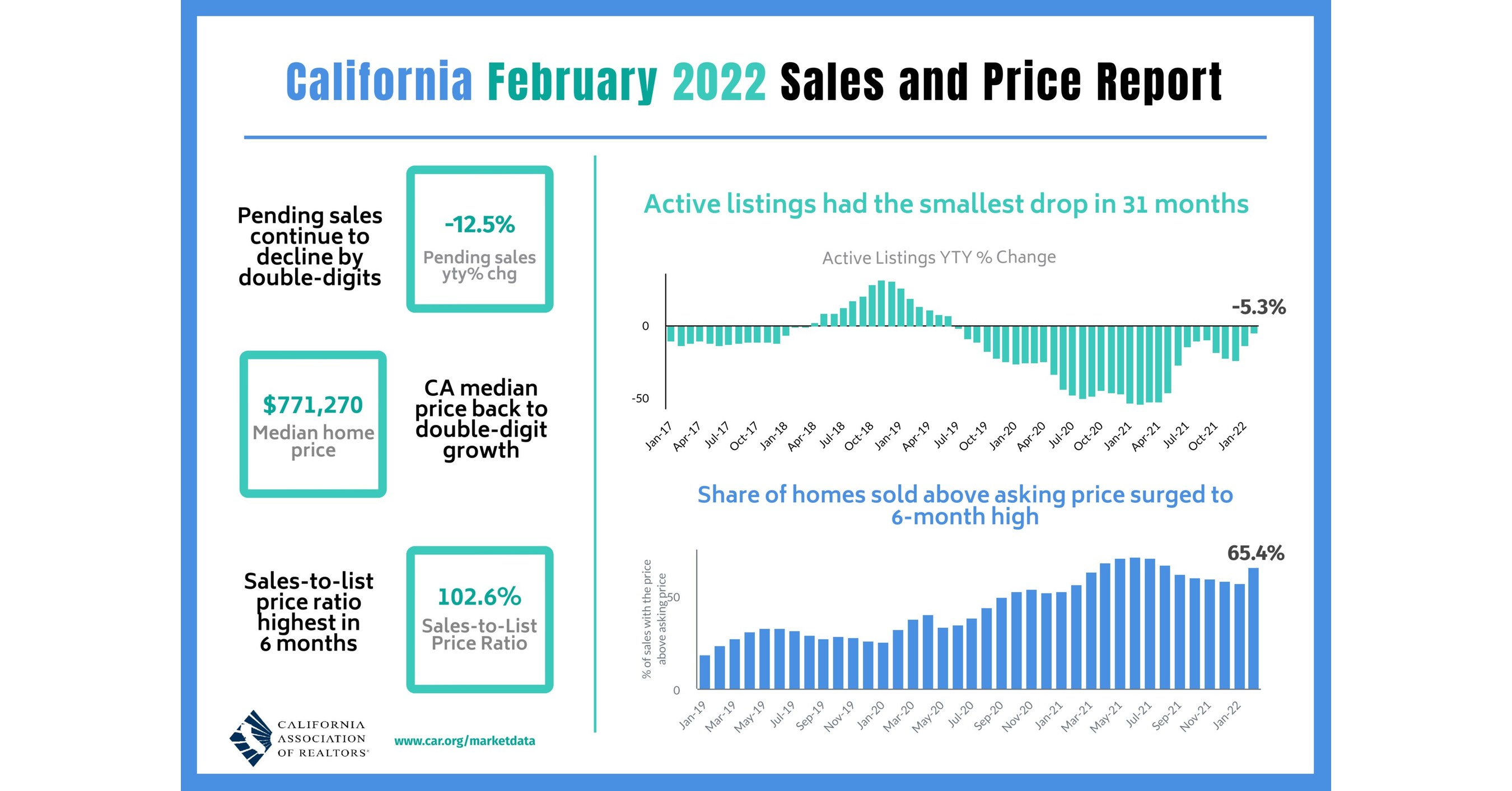

Closed escrow gross sales of present, single-family indifferent properties in California totaled a seasonally adjusted annualized charge of 424,640 in February, in line with data collected by C.A.R. from greater than 90 native REALTOR® associations and MLSs statewide. The statewide annualized gross sales determine represents what can be the overall variety of properties bought throughout 2022 if gross sales maintained the February tempo all year long. It’s adjusted to account for seasonal elements that usually affect residence gross sales.

February’s gross sales tempo was down 4.5 % on a month-to-month foundation from 444,540 in January and was down 8.2 % from a yr in the past, when 462,720 properties had been bought on an annualized foundation. The year-over-year gross sales lower was the eighth straight decline and the smallest in seven months.

“Regardless of greater mortgage charges, California’s housing market is holding up remarkably robust, with residence costs reaccelerating, market competitors rising and indicators that the listings crunch is thawing,” stated C.A.R. President Otto Catrina, a Bay Space actual property dealer and REALTOR®. “Potential consumers are profiting from still-low charges earlier than they transfer greater and getting a leap on competitors earlier than the beginning of the spring homebuying season.”

California residence costs continued to extend from the prior yr, selecting up momentum once more after slowing down for eight consecutive months. The statewide median value inched as much as $771,270 in February, up 0.7 % from January’s $765,610 and up 10.3 % from the $699,000 recorded in February 2021. The stronger-than-expected progress within the statewide median value is attributed partly to a change within the mixture of gross sales towards properties within the million-dollar value vary, as gross sales jumped in higher-priced areas such because the Central Coast and the San Francisco Bay Space.

“Whereas residence gross sales declined from each the earlier month and yr, February’s gross sales tempo was nonetheless the second highest gross sales degree for a February within the final 10 years and robust relative to pre-pandemic ranges of 2018 and 2019,” stated C.A.R. Vice President and Chief Economist Jordan Levine. “Nevertheless, the invasion of Ukraine has created geopolitical headwinds and pushed up inflation up a notch, which can maintain mortgage charges elevated and trigger the housing market to retreat amid the uncertainty.”

At an index of 67 in February, C.A.R.’s month-to-month Client Housing Sentiment Index dropped 2 factors from final month as shoppers acknowledged the present market challenges and felt more and more pessimistic about homebuying alternatives. Customers who thought it was a “Good time to purchase” dropped to 16 in February from 19 final month and from 28 factors final yr. Nonetheless, one in each 4 shoppers are holding out hope that will probably be simpler to discover a residence within the subsequent 12 months and practically two in each three imagine that residence costs will rise over the identical time period.

Different key factors from C.A.R.’s February 2022 resale housing report embrace:

- On the regional degree, all main areas besides the Central Valley recorded a lower in gross sales on a year-over-year foundation, however lower-priced areas continued to fare higher than higher-priced areas within the Golden State. The Central Coast area had the sharpest decline of all areas, with gross sales in February dropping 16.3 % from a yr in the past. To place issues into perspective although, housing demand was abnormally robust early final yr with gross sales in February 2021 surging 22.4 % from the prior yr. The San Francisco Bay Space and Southern California additionally skilled a double-digit or a close to double-digit gross sales lack of -13.7 % and -9.9 %, respectively in February. Residence gross sales within the Far North additionally dipped 8.5 %, however the tempo was barely higher than the aforementioned areas. The Central Valley was the one area with a gross sales acquire in February, rising 1.2 % from a yr in the past.

- Over 70 % of all counties tracked by C.A.R. skilled a dip in present residence gross sales from a yr in the past, with 24 counties declining greater than 10 % on a year-over-year foundation. With many properties destroyed by the Dixie Fireplace final summer time, Plumas had the biggest decline of all counties in February, falling 62.1 % from a yr in the past. Mariposa (-50.0 %), Amador (-35.2 %), and Mendocino (-32.7 %) had been three different counties in California that additionally skilled a gross sales drop of greater than 30 % final month. Counties with a gross sales decline from final yr had a median lower of -17.7 % in February. Fourteen counties skilled a gross sales acquire from final yr, with Yuba (65.3 %) surging essentially the most, adopted by Siskiyou (45.8 %) and Sutter (31.9 %).

- Residence costs continued to develop in all main areas within the state, with all 5 posting double-digit year-over-year good points of their median value. The San Francisco Bay Space recorded the best year-over-year value acquire at a 15.9 % improve, adopted by the Central Valley (14.8 %), Southern California (12.6 %), the Far North (11.9 %), and the Central Coast (10.1 %).

- Regardless of slower value progress resulting from rising mortgage charges, residence costs continued to extend throughout the state, with 24 California counties setting new file excessive median costs in February. All however three counties tracked by C.A.R. skilled a rise of their median value in February, with 38 of them surging by double-digits from a yr in the past. Santa Cruz had the largest year-over-year value improve at 30.4 %, adopted by Glenn (29.1 %) and Yolo (28.2 %). Three counties registered a median value decline from final yr, with Mono dropping essentially the most at -30.8 %, adopted by Santa Barbara (-10.6 %) and Mendocino (-4.8 %).

- California’s Unsold Stock Index (UII) rose in February as lively listings climbed from January to the best degree in three months. February’s UII was 2.0 months and a pair of.1 months in February 2021. The index signifies the variety of months it might take to promote the availability of properties in the marketplace on the present charge of gross sales.

- The median variety of days it took to promote a California single-family residence was 9 days in February and 10 days in February 2021.

- C.A.R.’s statewide sales-price-to-list-price ratio* was 102.6 % in February 2022 and 101.0 % in February 2021.

- The statewide common value per sq. foot** for an present single-family residence remained elevated. February’s value per sq. foot was $392, up from $338 in February a yr in the past.

- The 30-year, fixed-mortgage rate of interest averaged 3.76 % in February, up from 2.81 % in February 2021, in line with Freddie Mac. The five-year, adjustable mortgage rate of interest averaged 2.87 %, in comparison with 2.83 % in February 2021.

Observe: The County MLS median value and gross sales information within the tables are generated from a survey of greater than 90 associations of REALTORS® all through the state and symbolize statistics of present single-family indifferent properties solely. County gross sales information aren’t adjusted to account for seasonal elements that may affect residence gross sales. Actions in gross sales costs shouldn’t be interpreted as modifications in the price of an ordinary residence. The median value is the place half bought for extra and half bought for much less; medians are extra typical than common costs, that are skewed by a comparatively small share of transactions at both the decrease finish or the higher finish. Median costs will be influenced by modifications in value, in addition to modifications within the traits and the dimensions of properties bought. The change in median costs shouldn’t be construed as precise value modifications in particular properties.

*Gross sales-to-list-price ratio is an indicator that displays the negotiation energy of residence consumers and residential sellers beneath present market situations. The ratio is calculated by dividing the ultimate gross sales value of a property by its final listing value and is expressed as a proportion. A sales-to-list ratio with one hundred pc or above means that the property bought for greater than the listing value, and a ratio under one hundred pc signifies that the worth bought under the asking value.

**Value per sq. foot is a measure generally utilized by actual property brokers and brokers to find out how a lot a sq. foot of area a purchaser can pay for a property. It’s calculated because the sale value of the house divided by the variety of completed sq. ft. C.A.R. at present tracks price-per-square foot statistics for 50 counties.

Main the best way…® in California actual property for greater than 110 years, the CALIFORNIA ASSOCIATION OF REALTORS® (www.automotive.org) is among the largest state commerce organizations in america with greater than 217,000 members devoted to the development of professionalism in actual property. C.A.R. is headquartered in Los Angeles.

|

February 2022 County Gross sales and Value Exercise |

|||||||||

|

(Regional and apartment gross sales information not seasonally adjusted) |

|||||||||

|

February 2022 |

Median Offered Value of Current Single-Household Properties |

Gross sales |

|||||||

|

State/Area/County |

Feb. 2022 |

Jan. 2022 |

Feb. 2021 |

Value |

Value |

Gross sales |

Gross sales |

||

|

Calif. Single-family residence |

$771,270 |

$765,610 |

r |

$699,000 |

0.7% |

10.3% |

-4.5% |

-8.2% |

|

|

Calif. Condominium/Townhome |

$640,000 |

$600,000 |

$530,000 |

6.7% |

20.8% |

9.4% |

-11.2% |

||

|

Los Angeles Metro Space |

$725,000 |

$700,000 |

$649,000 |

3.6% |

11.7% |

-4.7% |

-10.9% |

||

|

Central Coast |

$912,250 |

$920,400 |

$828,500 |

-0.9% |

10.1% |

7.8% |

-16.3% |

||

|

Central Valley |

$465,000 |

$455,000 |

$405,000 |

2.2% |

14.8% |

-1.0% |

1.2% |

||

|

Far North |

$375,000 |

$380,000 |

$335,000 |

-1.3% |

11.9% |

-3.0% |

-8.5% |

||

|

Inland Empire |

$551,000 |

$539,000 |

$470,000 |

2.2% |

17.2% |

-5.0% |

-6.4% |

||

|

San Francisco Bay Space |

$1,335,000 |

$1,200,000 |

$1,151,500 |

11.3% |

15.9% |

6.6% |

-13.7% |

||

|

Southern California |

$760,000 |

$740,000 |

$675,000 |

2.7% |

12.6% |

-2.5% |

-9.9% |

||

|

San Francisco Bay Space |

|||||||||

|

Alameda |

$1,350,000 |

$1,250,000 |

$1,100,000 |

8.0% |

22.7% |

13.0% |

-9.4% |

||

|

Contra Costa |

$935,000 |

$829,000 |

$817,500 |

12.8% |

14.4% |

-4.3% |

-19.6% |

||

|

Marin |

$1,580,000 |

$1,450,000 |

$1,540,000 |

9.0% |

2.6% |

38.6% |

-22.5% |

||

|

Napa |

$1,034,500 |

$884,000 |

$931,500 |

17.0% |

11.1% |

19.2% |

-8.8% |

||

|

San Francisco |

$1,900,000 |

$1,630,000 |

$1,786,400 |

16.6% |

6.4% |

12.6% |

5.9% |

||

|

San Mateo |

$2,100,000 |

$2,000,000 |

$1,900,000 |

5.0% |

10.5% |

-0.5% |

-24.4% |

||

|

Santa Clara |

$1,820,000 |

$1,716,000 |

$1,486,250 |

6.1% |

22.5% |

9.9% |

-17.1% |

||

|

Solano |

$605,000 |

$579,000 |

$509,750 |

4.5% |

18.7% |

4.4% |

8.7% |

||

|

Sonoma |

$819,000 |

$789,000 |

$740,000 |

3.8% |

10.7% |

6.0% |

-15.2% |

||

|

Southern California |

|||||||||

|

Los Angeles |

$773,490 |

$800,960 |

$686,760 |

r |

-3.4% |

12.6% |

-4.5% |

-7.3% |

|

|

Orange |

$1,260,000 |

$1,195,000 |

$995,000 |

5.4% |

26.6% |

-5.1% |

-26.0% |

||

|

Riverside |

$605,030 |

$590,000 |

$519,500 |

2.5% |

16.5% |

-4.7% |

-8.2% |

||

|

San Bernardino |

$450,000 |

$450,000 |

$389,900 |

0.0% |

15.4% |

-5.3% |

-3.4% |

||

|

San Diego |

$888,000 |

$875,000 |

$765,000 |

1.5% |

16.1% |

7.3% |

-5.6% |

||

|

Ventura |

$887,500 |

$850,000 |

$750,000 |

4.4% |

18.3% |

-1.7% |

-16.8% |

||

|

Central Coast |

|||||||||

|

Monterey |

$885,000 |

$875,000 |

$820,000 |

1.1% |

7.9% |

-0.6% |

-12.8% |

||

|

San Luis Obispo |

$830,500 |

$851,500 |

$700,000 |

-2.5% |

18.6% |

23.3% |

-26.2% |

||

|

Santa Barbara |

$1,050,000 |

$912,500 |

$1,174,080 |

15.1% |

-10.6% |

1.1% |

-5.3% |

||

|

Santa Cruz |

$1,380,000 |

$1,257,500 |

$1,058,000 |

9.7% |

30.4% |

10.7% |

-18.4% |

||

|

Central Valley |

|||||||||

|

Fresno |

$405,000 |

$395,500 |

$350,000 |

2.4% |

15.7% |

5.3% |

7.2% |

||

|

Glenn |

$412,500 |

$332,500 |

$319,500 |

24.1% |

29.1% |

42.9% |

25.0% |

||

|

Kern |

$370,000 |

$367,000 |

$295,000 |

0.8% |

25.4% |

-3.3% |

-4.9% |

||

|

Kings |

$327,000 |

$322,500 |

$280,000 |

1.4% |

16.8% |

-13.6% |

-8.1% |

||

|

Madera |

$400,000 |

$394,000 |

$354,500 |

1.5% |

12.8% |

13.4% |

-0.8% |

||

|

Merced |

$390,000 |

$387,380 |

$318,750 |

0.7% |

22.4% |

-29.0% |

-6.6% |

||

|

Placer |

$675,000 |

$670,000 |

$599,500 |

0.7% |

12.6% |

2.1% |

-2.0% |

||

|

Sacramento |

$541,500 |

$524,000 |

$463,000 |

3.3% |

17.0% |

5.2% |

2.4% |

||

|

San Benito |

$860,000 |

$842,500 |

$700,000 |

2.1% |

22.9% |

2.8% |

8.8% |

||

|

San Joaquin |

$505,500 |

$499,950 |

$436,300 |

1.1% |

15.9% |

-6.2% |

2.8% |

||

|

Stanislaus |

$452,400 |

$450,000 |

$405,000 |

0.5% |

11.7% |

-16.3% |

-1.3% |

||

|

Tulare |

$338,000 |

$333,000 |

$288,500 |

1.5% |

17.2% |

-3.1% |

2.8% |

||

|

Far North |

|||||||||

|

Butte |

$426,500 |

$456,000 |

$397,000 |

-6.5% |

7.4% |

14.3% |

5.7% |

||

|

Lassen |

$239,000 |

$259,000 |

$208,250 |

-7.7% |

14.8% |

0.0% |

15.0% |

||

|

Plumas |

$339,000 |

$460,000 |

$329,500 |

-26.3% |

2.9% |

-59.3% |

-62.1% |

||

|

Shasta |

$375,000 |

$375,000 |

$329,950 |

0.0% |

13.7% |

-0.5% |

-12.1% |

||

|

Siskiyou |

$340,000 |

$296,000 |

$322,500 |

14.9% |

5.4% |

-16.7% |

45.8% |

||

|

Tehama |

$311,250 |

$359,000 |

$299,000 |

-13.3% |

4.1% |

-7.7% |

-26.5% |

||

|

Different Calif. Counties |

|||||||||

|

Amador |

$449,000 |

$400,000 |

$406,280 |

12.3% |

10.5% |

-10.3% |

-35.2% |

||

|

Calaveras |

$510,000 |

$467,500 |

$441,500 |

9.1% |

15.5% |

-3.8% |

1.3% |

||

|

Del Norte |

$390,000 |

$372,500 |

$359,000 |

4.7% |

8.6% |

-12.5% |

-26.3% |

||

|

El Dorado |

$730,000 |

$607,500 |

$577,500 |

20.2% |

26.4% |

6.6% |

-13.5% |

||

|

Humboldt |

$452,500 |

$425,000 |

$360,000 |

6.5% |

25.7% |

-21.4% |

-21.4% |

||

|

Lake |

$360,000 |

$349,900 |

$326,500 |

2.9% |

10.3% |

-6.2% |

-29.1% |

||

|

Mariposa |

$446,250 |

$350,000 |

$397,500 |

27.5% |

12.3% |

-25.0% |

-50.0% |

||

|

Mendocino |

$500,000 |

$508,500 |

$525,000 |

-1.7% |

-4.8% |

-13.2% |

-32.7% |

||

|

Mono |

$992,500 |

$950,000 |

$1,435,000 |

4.5% |

-30.8% |

-33.3% |

-28.6% |

||

|

Nevada |

$547,500 |

$550,000 |

$519,500 |

-0.5% |

5.4% |

-22.9% |

-22.2% |

||

|

Sutter |

$420,000 |

$415,000 |

$395,000 |

1.2% |

6.3% |

-13.9% |

31.9% |

||

|

Tuolumne |

$433,500 |

$386,750 |

$375,000 |

12.1% |

15.6% |

28.6% |

-11.1% |

||

|

Yolo |

$666,420 |

$542,500 |

$520,000 |

22.8% |

28.2% |

31.4% |

-13.2% |

||

|

Yuba |

$450,000 |

$402,500 |

$370,000 |

11.8% |

21.6% |

-8.0% |

65.3% |

||

|

February 2022 County Unsold Stock and Days on Market |

||||||||||

|

(Regional and apartment gross sales information not seasonally adjusted) |

||||||||||

|

February 2022 |

Unsold Stock Index |

Median Time on Market |

||||||||

|

State/Area/County |

Feb. 2022 |

Jan. 2022 |

Feb. 2021 |

Feb. 2022 |

Jan. 2022 |

Feb. 2021 |

||||

|

Calif. Single-family residence |

2.0 |

1.8 |

2.1 |

r |

9.0 |

12.0 |

10.0 |

|||

|

Calif. Condominium/Townhome |

1.8 |

1.8 |

2.3 |

r |

8.0 |

11.0 |

13.0 |

|||

|

Los Angeles Metro Space |

2.1 |

1.9 |

2.3 |

r |

10.0 |

13.0 |

11.0 |

|||

|

Central Coast |

2.0 |

2.1 |

2.5 |

r |

10.0 |

11.0 |

13.0 |

|||

|

Central Valley |

1.9 |

1.7 |

1.9 |

7.0 |

10.0 |

7.0 |

||||

|

Far North |

3.0 |

2.7 |

2.8 |

22.0 |

27.0 |

37.0 |

||||

|

Inland Empire |

2.0 |

1.9 |

2.1 |

r |

14.0 |

16.0 |

15.0 |

|||

|

San Francisco Bay Space |

1.9 |

1.6 |

2.1 |

9.0 |

12.0 |

10.0 |

||||

|

Southern California |

2.0 |

1.8 |

2.2 |

r |

9.0 |

12.0 |

10.0 |

|||

|

San Francisco Bay Space |

||||||||||

|

Alameda |

1.7 |

1.5 |

1.7 |

8.0 |

10.0 |

8.0 |

||||

|

Contra Costa |

1.9 |

1.4 |

1.7 |

8.0 |

9.0 |

7.5 |

||||

|

Marin |

1.6 |

2.0 |

2.1 |

10.0 |

29.0 |

22.0 |

||||

|

Napa |

3.1 |

3.4 |

3.8 |

30.0 |

47.5 |

38.0 |

||||

|

San Francisco |

2.4 |

2.0 |

2.3 |

r |

12.0 |

13.0 |

13.0 |

|||

|

San Mateo |

2.1 |

1.6 |

2.4 |

7.0 |

10.0 |

9.0 |

||||

|

Santa Clara |

2.0 |

1.6 |

2.2 |

7.0 |

7.0 |

8.0 |

||||

|

Solano |

1.4 |

1.3 |

1.6 |

24.0 |

32.5 |

29.0 |

||||

|

Sonoma |

2.2 |

1.9 |

3.0 |

27.0 |

42.0 |

38.0 |

||||

|

Southern California |

||||||||||

|

Los Angeles |

2.2 |

2.0 |

2.4 |

r |

10.0 |

13.0 |

10.0 |

|||

|

Orange |

2.0 |

1.6 |

2.4 |

r |

7.0 |

8.0 |

9.0 |

|||

|

Riverside |

1.9 |

1.8 |

2.1 |

r |

14.0 |

16.0 |

14.0 |

|||

|

San Bernardino |

2.1 |

2.1 |

2.1 |

r |

13.0 |

16.0 |

15.0 |

|||

|

San Diego |

1.5 |

1.5 |

1.8 |

7.0 |

9.0 |

7.0 |

||||

|

Ventura |

2.3 |

2.0 |

2.4 |

r |

20.0 |

20.0 |

24.0 |

|||

|

Central Coast |

||||||||||

|

Monterey |

2.2 |

2.1 |

2.8 |

10.0 |

10.0 |

14.0 |

||||

|

San Luis Obispo |

2.0 |

2.3 |

2.2 |

r |

9.0 |

9.0 |

12.0 |

|||

|

Santa Barbara |

1.9 |

1.9 |

2.4 |

10.0 |

12.0 |

13.0 |

||||

|

Santa Cruz |

2.2 |

2.0 |

2.5 |

9.0 |

13.5 |

14.5 |

||||

|

Central Valley |

||||||||||

|

Fresno |

2.0 |

1.9 |

2.0 |

7.0 |

9.0 |

7.0 |

||||

|

Glenn |

2.0 |

3.0 |

2.7 |

r |

14.0 |

7.5 |

12.5 |

|||

|

Kern |

1.9 |

1.7 |

2.2 |

8.0 |

9.0 |

9.0 |

||||

|

Kings |

2.3 |

2.1 |

2.7 |

7.0 |

10.0 |

6.0 |

||||

|

Madera |

2.8 |

3.1 |

2.4 |

12.0 |

17.0 |

10.0 |

||||

|

Merced |

2.5 |

1.5 |

2.4 |

r |

9.0 |

14.5 |

10.0 |

|||

|

Placer |

1.8 |

1.6 |

1.8 |

6.0 |

9.0 |

6.0 |

||||

|

Sacramento |

1.5 |

1.4 |

1.6 |

7.0 |

8.0 |

6.0 |

||||

|

San Benito |

2.4 |

2.2 |

3.3 |

19.0 |

12.0 |

11.0 |

||||

|

San Joaquin |

2.0 |

1.6 |

1.9 |

8.0 |

12.5 |

7.0 |

||||

|

Stanislaus |

1.9 |

1.4 |

1.9 |

r |

9.0 |

10.0 |

7.0 |

|||

|

Tulare |

1.9 |

1.9 |

2.0 |

12.0 |

11.0 |

11.5 |

||||

|

Far North |

||||||||||

|

Butte |

2.1 |

2.4 |

2.6 |

r |

7.0 |

14.5 |

13.5 |

|||

|

Lassen |

3.4 |

3.6 |

3.3 |

107.0 |

80.0 |

106.0 |

||||

|

Plumas |

8.7 |

3.1 |

4.7 |

124.0 |

127.0 |

96.0 |

||||

|

Shasta |

2.9 |

2.5 |

2.5 |

19.0 |

19.0 |

27.0 |

||||

|

Siskiyou |

3.9 |

3.5 |

4.8 |

66.5 |

39.0 |

44.0 |

||||

|

Tehama |

3.2 |

2.9 |

2.7 |

58.5 |

49.0 |

77.0 |

||||

|

Different Calif. Counties |

||||||||||

|

Amador |

3.1 |

2.3 |

2.2 |

r |

23.0 |

33.0 |

12.0 |

|||

|

Calaveras |

2.5 |

2.1 |

2.0 |

66.0 |

73.0 |

57.0 |

||||

|

Del Norte |

5.1 |

4.2 |

3.8 |

78.0 |

70.0 |

167.0 |

||||

|

El Dorado |

2.3 |

2.0 |

2.1 |

14.0 |

33.0 |

13.0 |

||||

|

Humboldt |

4.3 |

3.0 |

2.4 |

10.0 |

10.0 |

10.0 |

||||

|

Lake |

4.9 |

4.2 |

3.0 |

r |

41.0 |

39.0 |

35.5 |

|||

|

Mariposa |

6.4 |

4.3 |

2.1 |

r |

10.5 |

62.0 |

11.5 |

|||

|

Mendocino |

6.5 |

5.2 |

3.2 |

45.0 |

52.5 |

61.0 |

||||

|

Mono |

3.7 |

2.5 |

2.9 |

89.5 |

90.0 |

62.5 |

||||

|

Nevada |

3.2 |

2.3 |

2.5 |

r |

20.5 |

30.0 |

35.5 |

|||

|

Sutter |

1.7 |

1.2 |

1.8 |

10.0 |

8.0 |

10.0 |

||||

|

Tuolumne |

2.9 |

3.4 |

2.4 |

40.0 |

39.5 |

17.5 |

||||

|

Yolo |

1.6 |

1.8 |

1.7 |

r |

9.0 |

10.0 |

7.5 |

|||

|

Yuba |

1.9 |

1.5 |

2.2 |

8.0 |

11.0 |

12.0 |

||||

SOURCE CALIFORNIA ASSOCIATION OF REALTORS