/cloudfront-us-east-2.images.arcpublishing.com/reuters/GB3DRFHWLBP7ZNY2L7UAJGFLZQ.jpg&description=First-time+U.S.+dwelling+consumers+feeling+%E2%80%98defeated%E2%80%99+by+excessive+costs){kind=link}

/cloudfront-us-east-2.images.arcpublishing.com/reuters/GB3DRFHWLBP7ZNY2L7UAJGFLZQ.jpg)

March 15 (Reuters) – Brianna Lombardozzi lastly has her funds to some extent the place she may be capable of purchase a home. However she is not feeling nice about her odds.

Lombardozzi, 37, used her federal stimulus checks and different financial savings constructed up throughout the pandemic to pay down the vast majority of her bank card debt – a transfer that helped her credit score rating rise by virtually 100 factors.

However competitors is intense for properties in her worth vary of $175,000 to $225,000 in Central, South Carolina, and she or he has had 4 bids rejected over the previous month. Now with mortgage charges rising, she would not know if she’ll discover an inexpensive property earlier than her lease is up on the finish of Could.

Register now for FREE limitless entry to Reuters.com

“Proper now, I really feel a bit defeated,” mentioned Lombardozzi, who works in housing for a neighborhood college.

As dwelling costs soar, housing affordability is sinking to the bottom ranges since 2008 and first-time consumers – who have not benefited from rising dwelling values and are additionally dealing with rising rents – are being squeezed out.

First-time consumers accounted for 27% of present dwelling gross sales in January, in line with the Nationwide Affiliation of Realtors, close to 2014 ranges. With mortgage charges above 4%, across the highest in about three years, and anticipated to rise additional, consumers on tight budgets might wrestle much more to seek out properties they’ll afford.

AFFORDABILITY STRAINED

Demand for housing soared throughout the pandemic as consumers capitalized on record-low mortgage charges and distant staff sought extra dwelling house. Some individuals, like Lombardozzi, saved cash they might have usually spent on journey or eating out whereas a lot of the financial system was shut down, leaving them with more money to doubtlessly spend money on a house.

On the identical time, the variety of properties on the market plunged as some homeowners stayed put due to uncertainty and supply-chain disruptions and labor shortages slowed new dwelling building.

Whereas some imbalances are easing, the availability of properties on the market on the finish of January was at a document low – solely sufficient to final 1.6 months, NAR information reveals. That’s forcing consumers to compete over restricted listings and pushing costs increased. learn extra

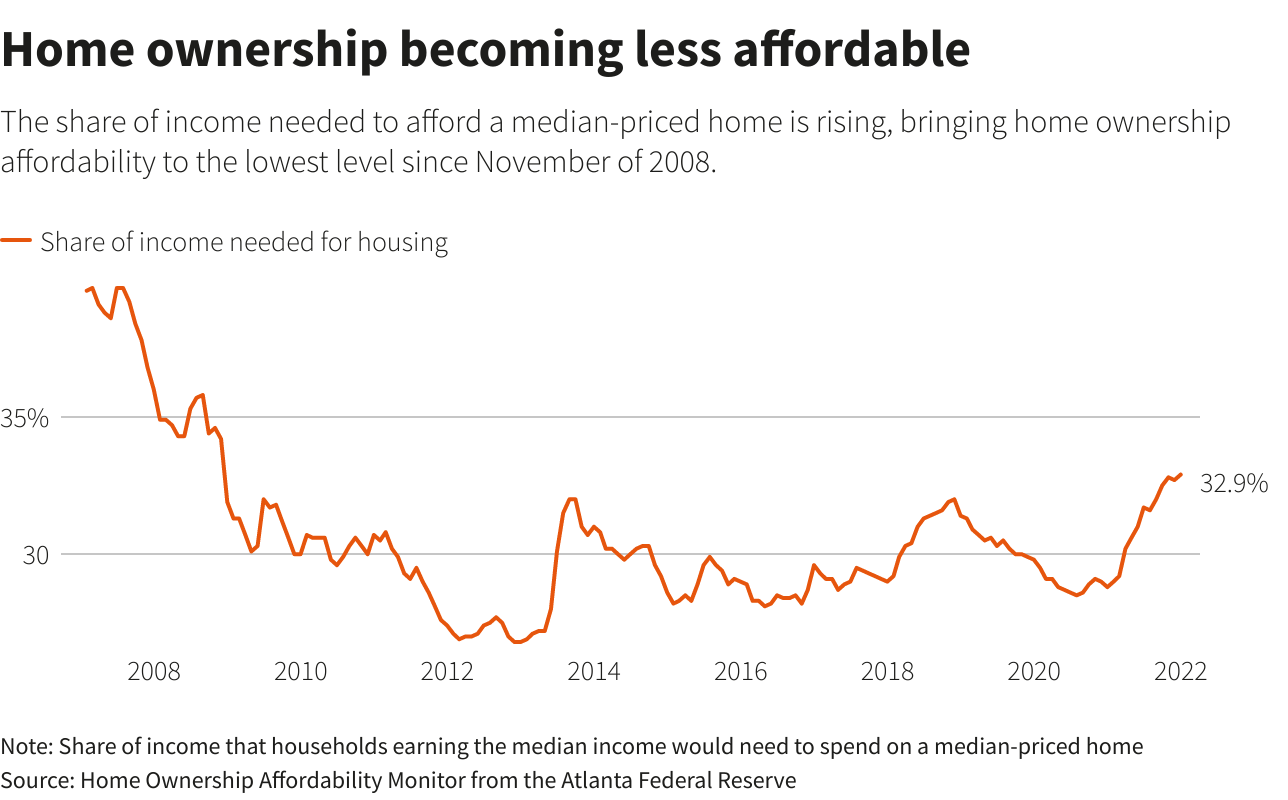

On the finish of 2021, housing affordability dropped to the bottom ranges since November of 2008, with households incomes the median revenue needing to spend almost 33% of their revenue to afford funds on a median-priced dwelling, in line with the Atlanta Federal Reserve. Housing is usually considered as inexpensive when households spend not more than 30% of their revenue on shelter.

Affordability could also be strained even additional by rising mortgage charges. Some individuals who had been pre-approved for a mortgage might discover they not qualify for a similar most mortgage quantity after mortgage charges rise, mentioned Jennifer Beeston, a senior vice chairman of mortgage lending for Assured Charge, a mortgage lender.

First-time consumers are already struggling to compete with all-cash provides, together with from institutional traders similar to private-equity funds, that are taking over a better share of purchases and are considered as much less dangerous by sellers, analysts say. Money purchases accounted for 27% of gross sales in January, up from 19% a yr earlier, in accordance NAR.

And a few new consumers are being outbid by individuals with sufficient money to pay above what a mortgage banker is prepared to lend, primarily based on the house’s appraised worth, mentioned Erica Barraza, an actual property dealer within the Seattle space.

BRACING FOR DISAPPOINTMENT

Many potential dwelling consumers discover they should improve their budgets or decrease their requirements simply to have an opportunity at a successful bid. Additionally they have to maneuver quick, viewing properties the day they go available on the market and making provides inside a day, or minutes after the viewing.

These situations are hitting morale: A survey by Fannie Mae discovered simply 29% of respondents assume it is a good time to purchase a house, close to a document low for a collection launched in 2010. “What I spend 50% of my time doing now’s pep talks,” mentioned Beeston, who works in mortgage lending.

Jason Harrison and Jamar Haggans are simply getting began with their home-buying search, however they’re already decreasing expectations.

Their seek for a three-bedroom, two-bathroom home in Kansas Metropolis, Missouri, priced beneath $450,000 turns up solely 10 to twenty new homes day by day. A lot of them promote inside a day or two – typically properly above the asking worth.

After reviewing the standard of properties listed, they upped their finances by $75,000 and are nervous about over-paying.

“My largest concern proper now…is that if we wish to get a house we will must pay greater than it is truly price,” mentioned Harrison, 36.

Harrison and Haggans usually are not prepared to waive dwelling inspections or value determinations, which they fear will make them much less interesting than consumers prepared to make these concessions. They hope extra individuals will checklist their properties within the spring.

Delaying a house search additionally has prices for consumers going through rising rents.

Lombardozzi, who misplaced at the very least one bid to an all-cash provide, estimates she has a few month to discover a dwelling earlier than she wants to begin searching for leases.

The home she’s been renting for six years was lately bought, and she or he says comparable leases are going for 20% to 40% greater than what she is paying now.

She first began trying to find properties in January, and Mortgage Bankers Affiliation information reveals home-loan prices have climbed roughly three-quarters of a share level in that window, decreasing how a lot she will borrow if she needs to maintain the month-to-month mortgage fee at a stage she will afford.

“By the point I’d truly get a suggestion accepted, what’s going to the charges have gone as much as?” she mentioned. “Will I simply not be capable of purchase a home interval?”

Register now for FREE limitless entry to Reuters.com

Reporting by Jonnelle Marte;

Modifying by Dan Burns and Andrea Ricci

Our Requirements: The Thomson Reuters Belief Ideas.