{kind=link}

Michael M. Santiago/Getty Photos Information

Many traders view the big U.S. cash middle banks as related and anticipate them to commerce in a pack. In actuality, although, every has a really completely different enterprise combine that manifests in very completely different outcomes for shareholders.

My favourite matrix for banks is the value to tangible guide worth (“TBV”) and return on tangible frequent fairness (“RoTCE”).

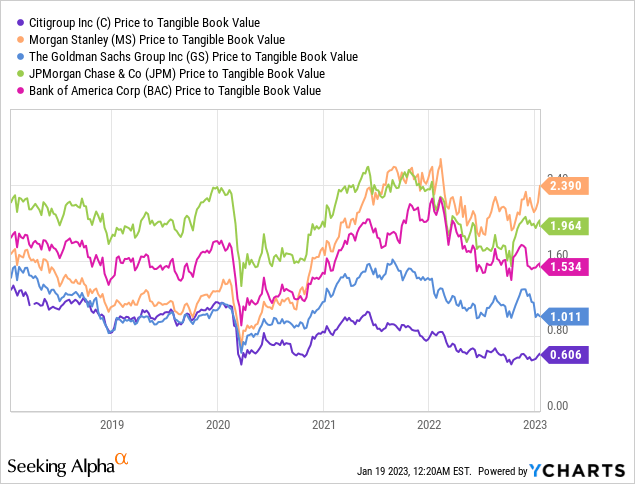

Contemplate the under chart for the big U.S. banks:

As you’ll be able to see from above, the valuation of those 5 massive U.S. banks diverges materially. For instance, Morgan Stanely (NYSE:MS) is ascribed a premium of ~4x to Citigroup (C). That is primarily a operate of the enterprise mannequin and blend that advanced over the past decade or so within the wake of the worldwide monetary disaster (“GFC”).

The GFC was a watershed second for the big banks as the principles of the sport have been rewritten by regulators which in flip utterly modified the returns profile of the completely different companies. Within the post-GFC world, the buying and selling companies (e.g. FICC) turned way more costly to run and attracted a a lot increased capital cost in contrast with their shopper banking cousins. On the flip facet, capital-light companies like wealth administration and asset administration turned way more engaging. Some administration groups understood this very early on (like James Morgan) whereas others like Citi and Goldman Sachs (NYSE:GS) missed the boat and are nonetheless trying to revamp their enterprise mannequin.

In different phrases, Popping out of the GFC, every financial institution made a strategic determination to double down on sure enterprise segments and deemphasize others. The present valuations of those banks are successfully a product of those capital allocation selections.

For instance, Citi opted to give attention to being a worldwide shopper financial institution working in a number of jurisdictions. Citi’s administration believed on the time, that rising markets’ GDP will develop quicker than its residence market within the U.S. and thus allotted capital and aligned its enterprise mannequin accordingly. It additionally doubled down on the company funding financial institution in addition to the worldwide Credit score Playing cards enterprise believing the latter ought to ship ROE within the excessive teenagers. Citi deemphasized wealth administration and offered its JV curiosity in Smith Barney to Morgan Stanley (MS). The technique has confirmed to be an unmitigated catastrophe and Citi’s new CEO has basically reversed that in a somewhat painful and protracted strategic revamp.

On this article, although, I’ll evaluate and distinction GS and MS and conclude which is the higher funding for 2023.

Table of Contents

The Response To This fall Earnings

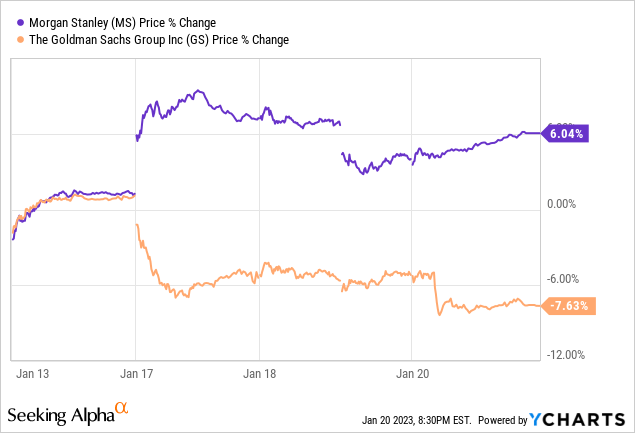

GS’s CEO, David Solomon, will need to have been fuming wanting on the divergent market response to the This fall earnings studies launched by MS and GS on the seventeenth of January (which by the way coincided along with his birthday).

The relative ~14% in relative efficiency this week displays each the plain success of MS’s give attention to the capital-light wealth administration enterprise in addition to GS’ over-reliance on unstable funding banking and the ill-advised journey into shopper banking.

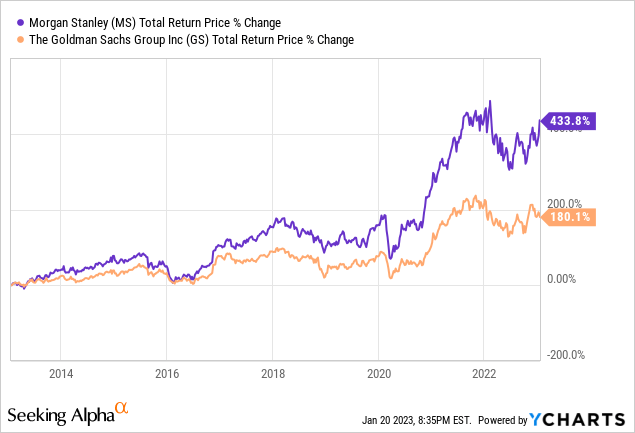

The longer-term image over the past 10 years tells the identical story:

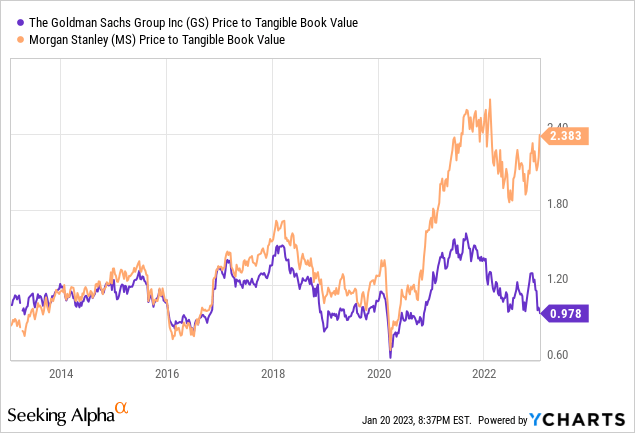

Viewing the identical chart by means of a price-to-book valuation:

The valuation of MS catapulted in recent times because the market rewards it for the success of its wealth administration technique that persistently delivers sturdy and powerful returns even in bear markets.

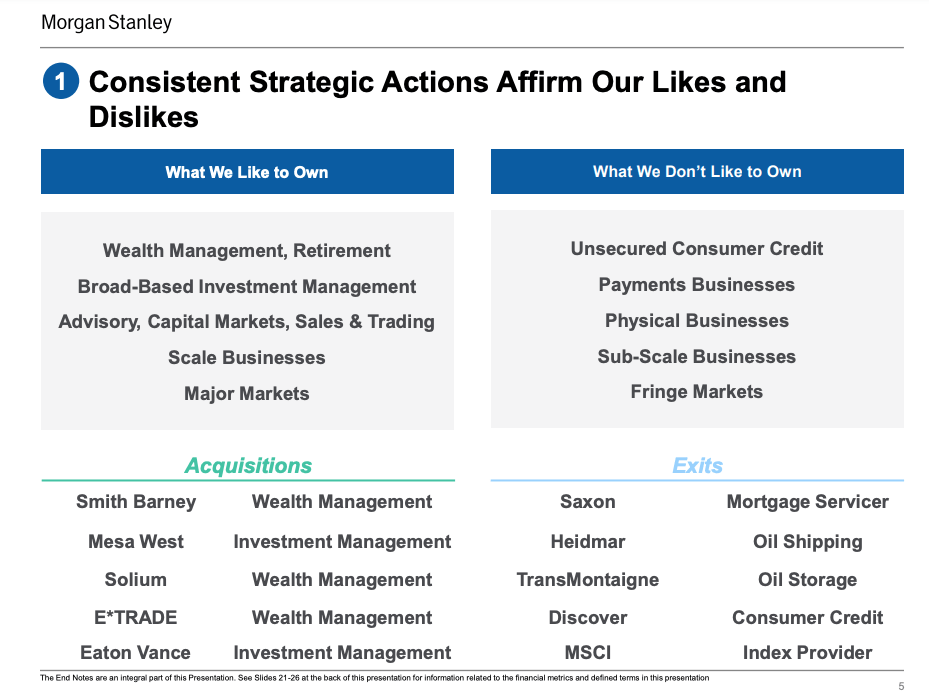

MS (maybe with a slight dig in direction of GS and different friends) has highlighted “our likes & dislikes” enterprise strains within the strategic replace presentation launched on the seventeenth Jan 2023:

MS Investor Relations

Clearly, MS is very centered on high quality companies and executing a transparent and coherent technique to develop the capital-light companies of wealth and asset administration.

GS, alternatively, is going through an id disaster. There is no such thing as a doubt, GS is the perfect class in funding banking and world markets division. The issue is that Mr. Market is not going to give excessive multiples for these companies as they’re each unstable and devour quite a lot of capital. As famous above, it is a operate of the post-GFC regulatory capital framework in addition to the Dodd-Frank Act.

Understanding Goldman Sachs

GS operates by means of 3 divisions:

- World Banking & Markets (“GBM”);

- Asset & Wealth Administration (“AWM”); and

- Platform Options (“PS”)

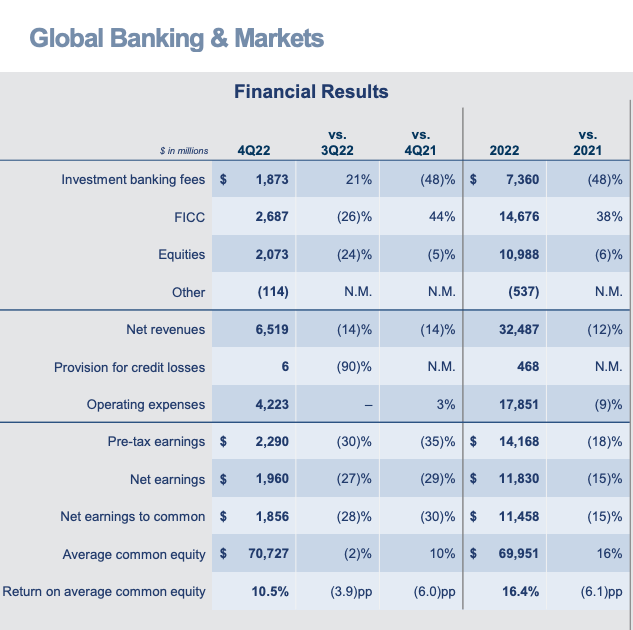

GBM is the biggest and includes the markets buying and selling enterprise (i.e. FICC and Equities buying and selling) as nicely the funding banking section (debt, fairness, and M&A advisory). The outcomes for 2022 are proven under:

GS Investor Relations

As can see above, GS allocates ~$70 billion of capital to this division and generated an ROE of 16.4% despite sturdy headwinds in funding banking the place the trade pockets was down greater than 50% because of the bear market in 2022 and quickly rising charges that trigger each debt and fairness issuances to freeze.

Make no mistake about this, these are unbelievable outcomes and it is rather clear that GS is the market chief when it comes to returns on this enterprise. I estimate that the likes of Citigroup and JPMorgan (JPM) would ordinarily generate solely about 10-12% ROE in these segments.

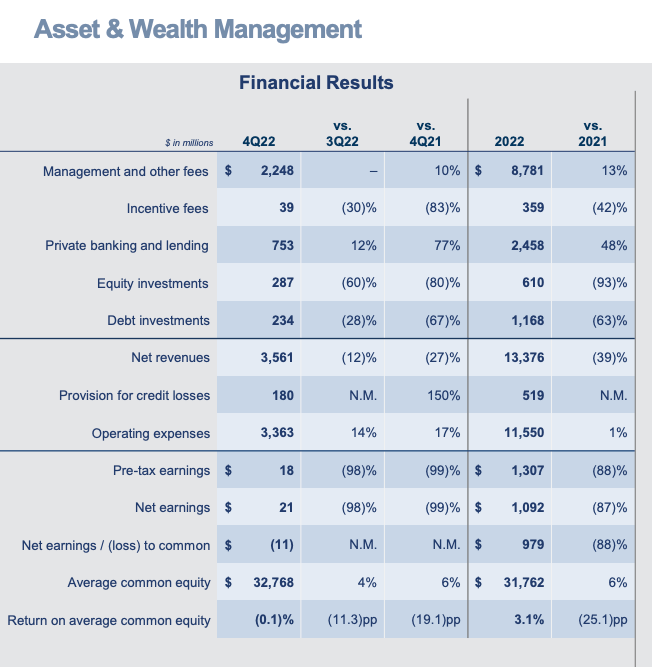

The AWM division includes wealth administration, asset administration, non-public banking enterprise in addition to GS’ proprietary fairness and debt investments (e.g. non-public fairness):

GS Investor Relations

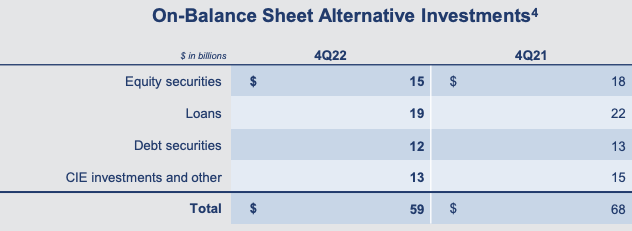

As can verify from above, the returns in 2022 have been removed from spectacular at solely 3.1% ROE. The primary offender is the proprietary investments (fairness and debt investments) that have been down 93% and 63% respectively because of the bear market valuations. The proprietary investments presently stand at $59 billion and devour a disproportionate quantity of capital, it’s a very capital-heavy enterprise mannequin. GS’s technique has been to work these down over time however the tempo has not been frantic, to say the least:

GS Investor Relations

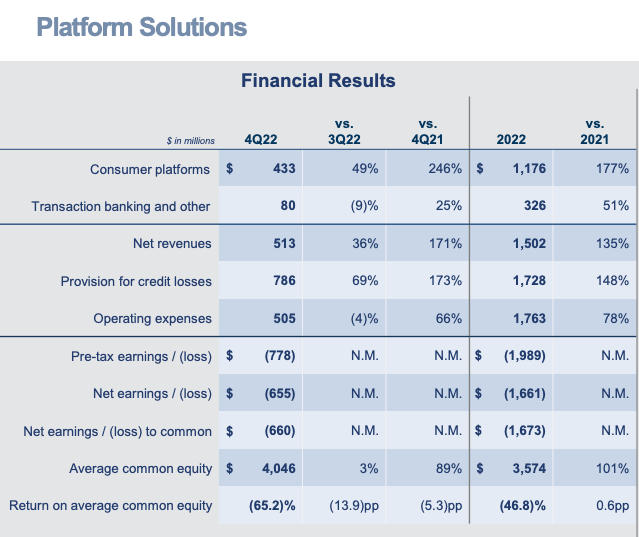

The third division is named Platform Options which includes the patron enterprise in addition to transaction banking. It solely consumes ~4b of capital and is roughly 3% of the financial institution, but produces disproportionate web revenue losses (~$1.7 billion) as might be seen under.

GS Investor Relations

GS’s technique is now to deemphasize the patron lending enterprise (Marcus), pivot to high-net-worth clientele, cut back prices and try to ship profitability. It’s retracting from the technique outlined beforehand by Lloyd Blankfein. The losses are too massive to bear and GS is in a rush to chop their losses and transfer on. Whereas the transaction banking enterprise is a pleasant one however nonetheless sub-scale and unlikely to maneuver the dial anytime quickly.

Understanding Morgan Stanely

MS is working by means of two massive divisions:

- Institutional Securities (“IS”)

- Wealth Administration (“WM”)

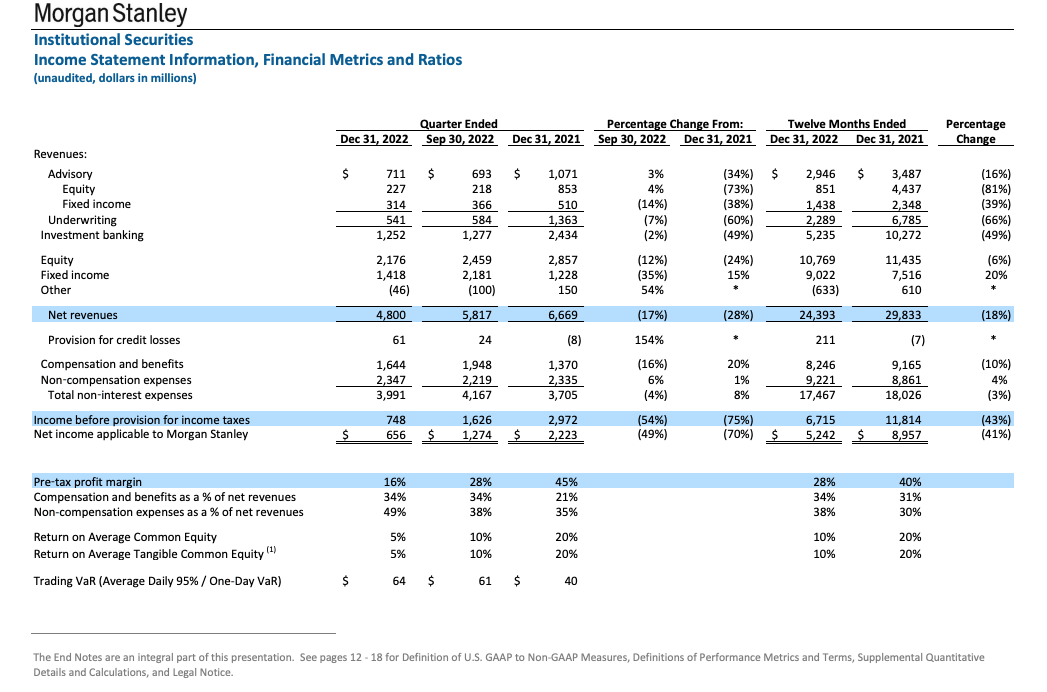

IS is much like GS’ GWB and includes each market buying and selling companies (FICC and Equities buying and selling) in addition to funding banking (debt, fairness, and M&A advisory). From a enterprise combine, MS is extra slanted in direction of Equities buying and selling versus FICC. As such, it isn’t shocking that its returns within the IS division in 2022 (at 10% ROE) have been considerably decrease than what GS delivered (16.4%).

MS Investor Relations

As might be seen from above, much like GS, the funding banking charges have been ~50% decrease in 2022 consistent with trade pockets reductions because of the bear market. Additionally, Equities buying and selling was decrease (-6%) year-on-year whereas FICC delivered 20% year-on-year progress. As famous above, MS’ enterprise combine is closely slanted towards Equities buying and selling and as such, underperformed on a relative foundation in comparison with friends who’re stronger in FICC buying and selling.

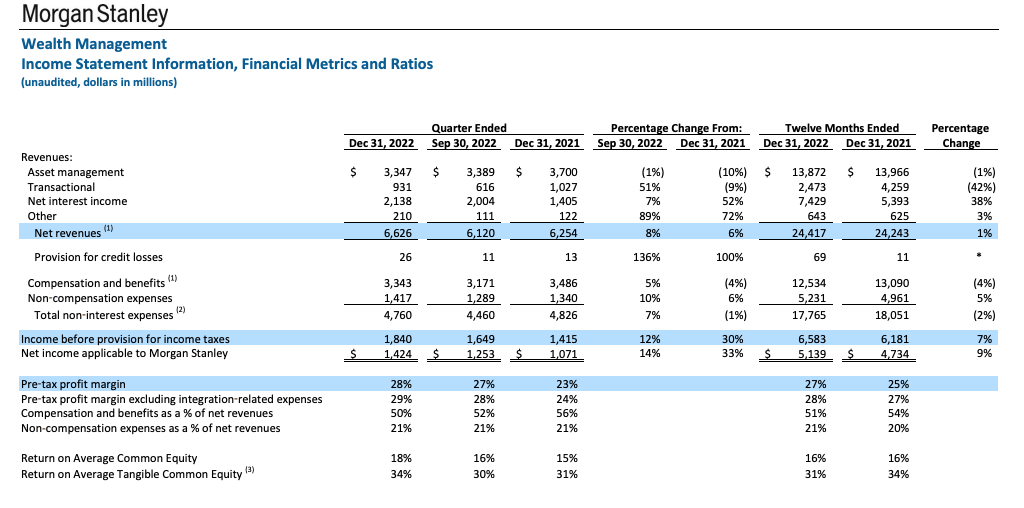

MS’s wealth administration division continued to ship in 2022 despite the deep bear markets in each bonds and equities. The WM division produced a 9% year-on-year progress in web revenue which is astounding given the macroeconomic circumstances prevailing in 2022.

MS Investor Relations

As might be seen above, WM is delivering >30% ROE which is an distinctive return for a financial institution. Curiously, the WM web revenue is roughly the identical because the IS division (~$5b of web revenue), nonetheless, makes use of a 3rd much less capital.

And that is actually the success story of MS and why it’s ascribed to such excessive multiples. The WM is delivering not solely distinctive returns (>30% ROE) however are additionally steady and sturdy in nearly all market circumstances.

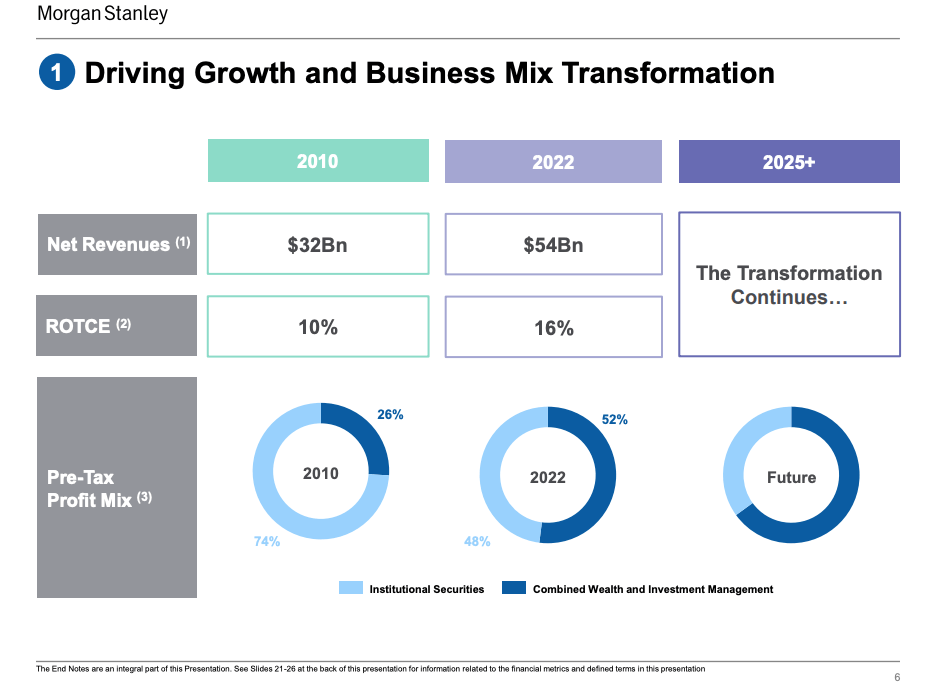

MS technique stays the identical and is all about growing the proportion of WM web revenue within the earnings combine. In 2022, it’s ~50%, and administration initiatives that it will likely be a lot increased within the medium time period as mirrored within the under slide from the technique replace:

MS Investor Relations

Dialogue: Which Financial institution Is The Higher Funding In 2023?

GS is the market chief in funding banking and buying and selling. Nonetheless, Mr. Market is not going to ascribe a excessive a number of even in growth occasions when it delivers astounding buying and selling outcomes. Just because it’s a capital-heavy and unstable enterprise. GS acknowledged this a number of years again and tried to develop different extra steady enterprise strains. It clearly did not execute the technique and all it has to point out for now are sub-scale companies and losses. The excellent news is that administration realizes this now and is chopping its losses shortly because it deemphasizes the patron companies.

Additionally it is clear that the one viable technique for GS is to double down on WM and third-party asset administration. GS has to develop this division each organically and inorganically and cut back its reliance on proprietary investments.

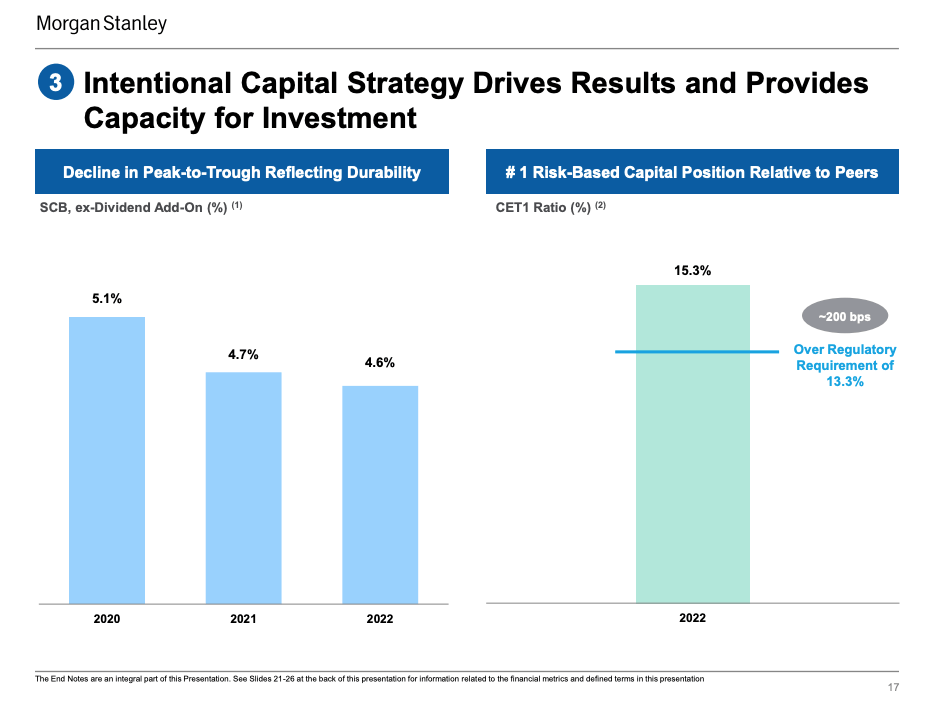

MS, alternatively, is executing a superb technique. The upper the enterprise combine shifts to wealth administration, the upper valuation Mr. Market will ascribe to its inventory. It presently holds $5.5T of shopper property and expects to nearly double it to $10T within the medium time period. It’s astounding that it elevated its profitability in 2022 when the fairness markets have been down ~20% and bonds have been down ~15% and a testomony to its distinctive enterprise mannequin.

The enterprise mannequin can also be very environment friendly from a capital utilization perspective. MS is delivering this profitability while working with 200 foundation factors capital buffer above its minimal requirement and is performing exceptionally nicely within the Fed’s CCAR stress assessments.

MS Investor Relations

Having mentioned that, at 2.4x tangible guide, MS is greater than pretty valued relative to its friends and particularly GS. It has at all times been a robust purchase sign to purchase GS the place it traded under tangible guide.

It’s true that a lot of GS’s issues are enterprise mannequin associated and considerably self-inflicted. Nonetheless, I’m assured administration might be laser-focused on fixing this. 2022 has been a troublesome 12 months for GS and returns have been damage by each losses within the shopper platforms in addition to unfavorable marks within the proprietary debt and fairness investments. The latter is unlikely to recur. On a normalized foundation, one would anticipate GS to ship mid-teens ROE. The upside or game-changer will manifest if it might probably severely develop the asset and wealth administration division. GS has a number of the greatest skills within the trade, I’d not guess in opposition to it.

Remaining ideas

The resiliency of the banking trade and enterprise mannequin is nothing wanting astounding (but I’m not shocked) given the macro circumstances prevailing in 2022.

In a deep bear market, MS and GS delivered 15% and 10% ROE respectively. GS nonetheless delivered 10% ROE despite unfavorable marks on proprietary investments and loss-making shopper division to the tune of $1.7 billion. MS wealth administration division delivered 9% year-on-year progress the place each the fairness and bond markets have been deep within the pink. These are distinctive outcomes.

MS has clearly a superior enterprise mannequin in comparison with GS however is pretty valued on a relative foundation. GS is buying and selling decrease than tangible guide worth as I write this text. Partly, this is because of its enterprise mannequin which is way more unstable however I consider administration can repair it within the medium time period. The important thing stays inorganic acquisitions within the asset and wealth administration division(much like the trail MS has taken). GS has a number of the smartest skills on Wall Road, to me, the chance/reward is very engaging at present valuations. GS will maintain its traders’ day on the twenty fifth of February, I anticipate it to disclose the refreshed technique. I’ve little doubt, it will likely be centered on the asset and wealth administration division progress.

As such, I charge GS as a robust purchase now. I additionally completely love the MS enterprise mannequin and charge it as a purchase provided that it’s pretty valued on a relative foundation to friends.