{kind=link}

Supply: Callahan’s Peer-to-Peer AnalyticsShare balances at credit score unions elevated 12.7% over the 2021 calendar yr, topping $1.8 trillion for the primary time ever within the fourth quarter and greater than double trade totals from a decade in the past. Nonetheless, deposit development has slowed from pandemic peaks. Share balances elevated 2.4% quarter-over-quarter, which was above the historic norm however effectively under the quarterly charges realized all through the pandemic. It’s not a shock that share development is waning in comparison with 2020, when unprecedented fiscal and financial stimulus drove hundreds of thousands of {dollars} into member share accounts, a lot of which sat ready for financial reopening. These shares created a surge in liquidity at many credit score unions, resulting in compressed trade curiosity spreads. Coming into 2022, the trade’s outlook is extra optimistic. Lending is at file highs – particularly within the client house – as demand has allowed credit score unions to repurpose a few of these new shares into productive loans. Nonetheless, whereas steadiness sheets could also be exhibiting indicators of stabilization, the massive inflow of funds in 2020 nonetheless poses ongoing macroeconomic challenges within the current day – particularly, inflation.

In latest months, markets have been centered on the Federal Reserve and its response to inflation. The December Federal Open Market Committee assembly confirmed the widespread expectation that tapering would finish in March, and three charge hikes have been forecast in 2022. The January FOMC assembly was much more eventful, with the Fed signaling that 5 charge hikes is now the consensus expectation for 2022, and the door was left open for much more. If realized, these will increase would push the Federal Funds charge to the 1.25%-1.50% vary in a comparatively brief time frame.

After being late to confess that top Shopper Worth Index inflation information was, in actual fact, not transitory, the Federal Reserve finds itself behind within the inflation administration battle. CPI studies have confirmed rising costs with every passing month, putting pressure on cost-of-living bills for customers. Elevating charges and proscribing the expansion of the cash provide are the financial instruments obtainable to the Federal Reserve to combat these inflationary pressures. Nonetheless, limiting the circulation of “straightforward” cash dangers asset worth crashes – notably within the fairness and actual property markets – and the potential for a full-blown recession. The financial shocks of the COVID-19 pandemic and prior short-term financial and monetary responses have left policymakers caught between a proverbial rock and a tough place. Markets and the general public at giant eagerly await additional alerts as to what the Fed will do relating to charge modifications, in addition to any plans for its practically $9 trillion steadiness sheet. The bond market can be watching intently for any indication of when and the way it plans to normalize, as tightening faster than anticipated could be unhealthy information for a lot of funding portfolios.

Cash Flows to Authorities Obligations

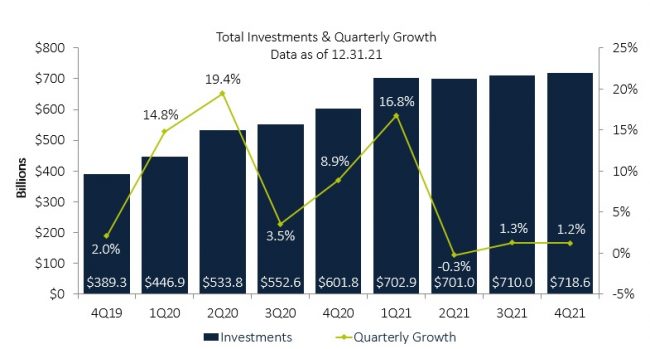

Money and safety balances at U.S. credit score unions elevated $8.7 billion since September to complete the yr at $718.6 billion. A sturdy 3.4% improve in securities and investments was partially offset by a 1.1% decline in money balances, as cooperatives repurposed liquidity into greater yielding belongings.

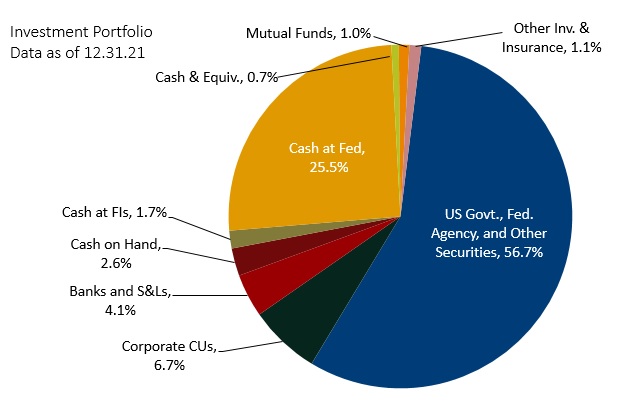

In greenback phrases, credit score union money balances declined $2.8 billion to complete $263.2 billion at year-end. They utilized the money to fulfill rebounding mortgage demand and to spend money on securities and investments; balances of the latter expanded $15.1 billion throughout the quarter. Money now includes simply 36.4% of complete investments, a 1.0 proportion level drop for the reason that finish of September. Damaged out into subcategories and holding areas, practically all money holdings declined on a quarterly foundation. Money equivalents and money available have been the biggest culprits, declining 18.9% and eight.4%, respectively. Money balances held on the Federal Reserve have been the one money holding class to broaden since September, up simply 0.3% to $183.8 billion.

Practically all development in trade funding portfolios got here within the securities house. U.S. authorities obligations and Federal company non-mortgage-backed safety investments acquired the majority of the money from credit score unions. Authorities obligation balances gained $6.6 billion, good for a 16.7% quarterly improve. The multi-year streak of Federal company MBS being the selection funding for credit score unions ended within the fourth quarter. Company MBS balances eked out a modest 0.2% improve however haven’t had a big improve for the reason that second quarter of 2021.

The flood of funding into authorities and company securities pushed this class to 56.7% of the entire credit score union funding portfolio, up from 55.5% final quarter. Mutual funds make up 1.0% of the portfolio, unchanged from September.

Supply: Callahan’s Peer-to-Peer Analytics

Supply: Callahan’s Peer-to-Peer AnalyticsStomach of the Curve Sees Inflows

Mounted revenue yields responded to the Fed’s dedication to lift charges by flattening throughout the fourth quarter and are actually again to ranges just like the beginning of the yr. The unfold between the two-year and 10-year Treasury notes declined to 78 foundation factors after reaching 129 foundation factors as not too long ago as October through the Delta variant scare. The five-year be aware elevated 10 foundation factors within the month of December to succeed in 1.26%.

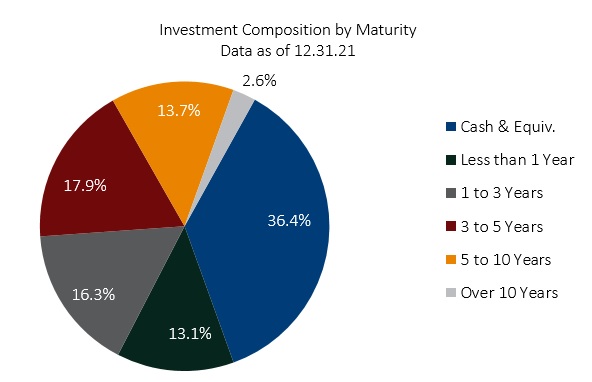

Credit score union funding managers took benefit of those shifts within the yield curve within the fourth quarter, by and enormous shifting portfolios from money into medium- and long-term securities. Particularly, the three-to-five-year maturity class elevated on the biggest charge of any time period group within the trade’s funding portfolio since September, up 6.9% – or $8.2 billion over the three months. For the complete yr of 2021, $53.3 billion piled into this maturity phase, an annual development charge of 70.9%. Comprising 17.9% of funding portfolios, three-to-five-year phrases are actually the second largest portion of investments after money. The five-to-10-year maturity group expanded 3.9% quarterly – and 81.3% yearly – and now makes up 13.7% of portfolios versus 9.0% a yr in the past. In all, credit score unions pulled away from low-yield, short-term securities over the previous few quarters in favor of those three-to-10-year phrases.

Supply: Callahan’s Peer-to-Peer Analytics

Supply: Callahan’s Peer-to-Peer Analytics Jay Johnson

Jay JohnsonJay Johnson is President of Callahan Monetary Companies, Distributor of the Belief for Credit score Unions, in Washington, D.C.