{kind=link}

Editor’s observe: This text is the primary in a three-part sequence. Plain textual content represents the writing of Greg Foss, whereas italicized copy represents the writing of Jason Sansone.

In February 2021, I printed the first model of this text (discover an govt abstract right here). Whereas it obtained some very optimistic suggestions, it additionally obtained numerous questions, notably with respect to how bonds are priced. Accordingly, I wished to replace the analysis to incorporate the latest market information, in addition to to clear up among the tougher ideas. I overlook that math could be imposing for most individuals, but since bonds and credit score devices are fiat contracts, bonds and credit score devices are pure math.

During the last yr, I’ve joined forces with an unimaginable staff of like-minded Bitcoiners and collectively we endeavor to unfold basic data about monetary markets and Bitcoin. The staff is called “The Wanting Glass” and consists of individuals with various origins, ages and experience. We’re involved residents who need to assist make a distinction for the longer term, a future that we consider wants to include a sound type of cash. That cash is bitcoin.

Instantly after I “met” Greg (listening to a podcast), I reached out to him on Twitter, and defined that, though I beloved what he needed to say, I solely understood about 10% of it. I requested if he may counsel any supplemental instructional materials and he despatched me a replica of his article, “Why Each Fastened Revenue Investor Wants To Think about Bitcoin As Portfolio Insurance coverage.” Thanks, sir. I now suppose I perceive even much less…

Lengthy story brief, and after a couple of exchanges, Greg and I rapidly turned pals. Belief me once I let you know that he’s pretty much as good and real of a human being as he appears. As he talked about above, we rapidly realized our shared imaginative and prescient and arranged “The Wanting Glass” staff. Regardless, I nonetheless don’t perceive most of what he says. I need to consider it’s all true, like when he states with conviction that, “Bitcoin is one of the best uneven commerce I’ve seen in my 32 years of buying and selling danger.”

However, as these of us within the Bitcoin neighborhood know, you must do your personal analysis.

Thus, the purpose is just not whether or not you presently perceive what he says, however reasonably, are you prepared to do the work in an effort to perceive? Don’t belief. Confirm.

What follows is my try and confirm and clarify what Greg is saying. He has written the plain textual content content material, whereas I’ve written the interposed italicized content material in an effort to assist translate his message for these of us who don’t communicate the identical language. The rabbit gap is certainly deep… let’s dive in.

Table of Contents

Credibility

That is my second try and hyperlink my expertise in my 32-year profession within the credit score markets with the great thing about Bitcoin. Very merely, Bitcoin is a very powerful monetary innovation and expertise that I’ve seen in my profession, a profession which I consider qualifies me to have an knowledgeable opinion.

What I deliver to the dialogue is an enormous expertise in danger administration and survival within the credit score markets. I survived as a result of I tailored. If I noticed I had made a mistake, I exited a commerce and even reversed a place. I consider my buying and selling expertise is considerably distinctive in Canada. I believe the assorted cycles I’ve lived by give me the knowledge to opine on why Bitcoin is such an vital consideration for each mounted earnings and credit score portfolio. The underside line is: I by no means cease studying, and I hope the identical for all of you… The world is dynamic.

Opposite to Greg, I’ve by no means “sat in a danger chair” or traded credit score markets. However I do perceive danger. I’m an orthopedic trauma surgeon. If you happen to fall off of a roof or get crushed in a automotive wreck and shatter your femur, pelvis, forearm, and so on., I’m the man you meet. Does this make me an skilled in credit score, Bitcoin or buying and selling? No. What I deliver to the dialogue is the power to take advanced conditions, break them all the way down to their foundational ideas, apply first-principle considering and act with conviction. I thrive in chaotic environments the place adapting in actual time can imply life or loss of life. The underside line is: I by no means cease studying. The world is dynamic. Sound acquainted?

Profession Highlights

Latin American Debt Disaster

I labored at Royal Financial institution of Canada (RBC), Canada’s largest Financial institution, in 1988 when my job was to cost C$900 million of Mexican debt for swap into Brady bonds. Right now, RBC was bancrupt. So have been all cash heart banks, therefore the Brady Plan. The small print aren’t essentially vital, however briefly, RBC’s guide worth of fairness was lower than the write-down that might be required, on a mark-to-market foundation, on its lesser-developed international locations (LDC) mortgage guide.

A quick clarification is required right here: First, it’s crucial to know some fundamental ideas centered round “guide worth of fairness.” What this refers to is the stability sheet of an entity (on this case, banks). In brief, “stability” is achieved when belongings equal liabilities and fairness.

Assume first a couple of home. Let’s say you bought the house for $500,000. To take action, you made a $100,000 down cost and took out a mortgage from the financial institution for $400,000. Your stability sheet would seem as follows:

| Belongings | Liabilities |

|---|---|

|

$500,000 home |

$400,000 mortgage |

|

Fairness |

|

|

$100,000 down cost |

Let’s now say, for argument’s sake, your private stability sheet is marked to market. Which means every single day, your home is re-appraised at its market worth. For instance, on Monday it is likely to be price $507,030, on Tuesday $503,780, and so on. You get the purpose. On Monday and Tuesday, in an effort to “stability,” your stability sheet displays this appreciation in worth (of your private home) by accruing it to your fairness. Good for you.

Nonetheless, what occurs whether it is appraised at $496,840 on Wednesday? The stability sheet, now, has an issue, as your belongings equal $496,840, whereas your liabilities plus fairness equals $500,000. What do you do? You would stability the equation by depositing $3,160 right into a checking account and holding it as money. Phew, now your stability sheet balances, however you wanted to provide you with $3,160 so as to take action. This was, at greatest, an inconvenience. Fortunately, in the true world, nobody’s private stability sheet is marked to market.

Let’s now undergo the identical train with a financial institution, particularly the Royal Financial institution of Canada in 1988 which, as Greg mentions, was levered 25 occasions relative to its guide worth of fairness. In simplistic phrases, its stability sheet would have seemed one thing like this:

| Belongings | Liabilities |

|---|---|

|

$900 million LDC loans |

$865.4 million |

|

Fairness |

|

|

$34.6 million |

And sadly for banks, their stability sheets are marked to market — not on an accounting foundation, however implicitly by “good” fairness analysts. So, what occurs if a string of defaults happens inside the pool of LDC loans, such that the financial institution won’t ever see 1% of the $900 million owed to it? Maybe this can be a salvageable scenario… simply add $9 million to the belongings as money. However what if 10% of the $900 million mortgage guide defaulted? What if the financial institution needed to “restructure” practically the entire $900 million mortgage guide in an effort to get well any of it and it re-negotiated with the LDC purchasers to recapture solely $600 million of the unique $900 million? That’s an terrible lot of money to provide you with in an effort to preserve “stability.”

Regardless, this was a scary discovery. Most, if not all, monetary analysts on the fairness desks had not performed this straightforward calculation as a result of they didn’t perceive credit score. They only felt, like most Canadians do, that the large six Canadian banks are too large to fail. There may be an implicit Canadian authorities backstop. That’s true, however how would the federal government backstop it? Print fiat {dollars} out of skinny air. At the moment, the answer was gold (since Bitcoin didn’t but exist).

Nice Monetary Disaster (GFC)

Notice: This part might not make a lot sense now… we’ll break all of it down in future sections. Concern not.

My expertise with bancrupt cash heart banks in 1988 could be re-experienced in 2008 to 2009 when LIBOR charges and different counterparty danger measures shot by the roof previous to fairness markets smelling the rat. Once more, in late 2007, fairness markets rallied to new highs on Federal Reserve price cuts whereas the short-term industrial paper markets have been shut. The banks knew there was credit score contagion looming they usually stopped funding one another, a traditional warning sign.

I labored at GMP Funding Administration (GMPIM), a hedge fund, in 2008 to 2009 within the depths of the GFC. My accomplice was Michael Wekerle, who is without doubt one of the most colourful and skilled fairness merchants in Canada. He is aware of danger, and he rapidly understood that there was no level in taking lengthy positions in most equities till the credit score markets behaved. We turned a credit-focused fund, and acquired up tons of of hundreds of thousands of {dollars} of distressed Canadian debt in firms like Nova Chemical substances, Teck, Nortel and TD Financial institution within the U.S. markets, and hedged by shorting the fairness which traded largely in Canada.

“Hedged by shorting the fairness…” Huh? The idea of “hedging” is international to many retail buyers and it deserves a short clarification. Akin to “hedging your bets,” it includes successfully insuring your self towards a potential catastrophic end result within the markets. Utilizing the above instance, “shopping for distressed debt” means you’re buying the bonds of an organization that will not be capable of honor their debt obligations as a result of you’ll be able to purchase the appropriate to that debt principal payout (at maturity) at a fraction of the fee. This can be a nice funding assuming the corporate doesn’t default. However what if it does? Your “hedge” is to promote the fairness brief. This brief sale permits you to revenue if the corporate have been to enter chapter. This is only one instance of a hedging place. Different examples abound.

Nonetheless, this cross-border arbitrage was large, and Canadian fairness accounts had little or no thought why their fairness was relentlessly promoting off. I bear in mind one commerce that was 100% danger free, and thus introduced an infinite return on capital. It concerned Nova Chemical substances’ short-term debt, and put choices. Once more, the small print aren’t vital. Our CIO, Jason Marks (a Harvard College MBA graduate), believed in environment friendly markets and couldn’t consider I had discovered a risk-free commerce with large absolute return potential. Nonetheless, to his credit score, once I confirmed him my buying and selling blotter, after which requested “how a lot can I do?” (for danger restrict issues), his reply was lovely: “Do infinity.” Certainly, there may be large worth to adapting in a dynamic world.

At GMPIM, we additionally launched into the defining commerce of my profession. It concerned restructured asset-backed industrial paper (ABCP) notes. In brief, we traded over C$10 billion of the notes, from a low value of 20 cents on the greenback, proper as much as full restoration worth of 100 cents on the greenback. Uneven trades outline careers, and ABCP was one of the best uneven commerce versus danger I had seen up till that time in my profession.

COVID-19 Disaster

After which there was 2020… This time, the Fed did one thing completely new on the quantitative easing (QE) entrance: it began shopping for company credit score. Do you suppose the Fed was shopping for company credit score simply to grease the lending runway? Completely not. It was shopping for as a result of hugely-widening yield spreads (inflicting the worth of credit score belongings to lower, see stability sheet clarification above) would have meant banks have been as soon as once more bancrupt in 2020. Dangerous enterprise, that banking… good factor there’s a authorities backstop. Print, print, print… Answer: Bitcoin.

Quantitative easing (QE)? Most individuals don’t perceive what the Federal Reserve (“Fed”) is definitely doing behind the scenes, not to mention what QE is. There’s a large quantity of nuance right here and there are only a few individuals who really perceive this establishment absolutely (I, for one, am not claiming to be an skilled). Regardless, the Federal Reserve was initially established to resolve inelasticity considerations round nationwide financial institution forex. Via matches and begins, its position has modified dramatically through the years, and it now purports to behave in accordance with its mandates, together with:

- Goal a secure inflation price of two%; and,

- Keep full employment within the U.S. financial system

If these sound nebulous, it’s as a result of they’re. But the argument might be made that the Fed now has successfully reworked into an entity that helps the debt-based international financial system and prevents a deflationary collapse. How does it do that? Via many advanced processes with high-brow names, however successfully, the Fed enters the open market and purchases belongings in an effort to forestall a collapse of their worth. That is known as QE. And as you now know from the stability sheet dialogue above, a collapse within the mark-to-market worth of belongings wreaks havoc on the monetary system’s “plumbing.” How does the Fed afford to buy these belongings? It prints the cash wanted to purchase them.

The GFC transferred extra leverage within the monetary system onto the stability sheets of governments. Maybe there was no selection, however there isn’t any query that within the ensuing decade, we had the prospect to pay down the money owed that we had pulled ahead. We didn’t do this. Deficit spending elevated, QE was employed every time there was a touch of monetary uncertainty, and now, for my part, it’s too late. It’s pure arithmetic.

Sadly, most individuals (and buyers) are intimidated by math. They like to depend on subjective opinions and comforting assurances from politicians and central authorities that it’s okay to print “cash” out of skinny air. I consider the credit score markets could have a really completely different response to this indiscriminate printing, and this might occur briefly order. We must be ready, and we have to perceive why. “Slowly, then immediately” is a actuality in credit score markets… Danger occurs quick.

Again To (Bond) College

As I discussed above, uneven trades outline careers. Bitcoin is one of the best uneven commerce I’ve ever seen. Earlier than I make such a big declare, although, I had higher clarify why.

I first tried to take action one yr in the past, and you’ve got supplied me with questions and suggestions in order that Jason and I can refine the pitch. Collectively, we’ve got crafted a doc that I’d be comfy presenting to any fixed-income investor, massive or small, to elucidate why bitcoin must be embraced as a form of portfolio insurance coverage.

Basically, I argue that proudly owning bitcoin doesn’t improve portfolio danger, it reduces it. You’re really taking extra danger by not proudly owning bitcoin than you’re when you’ve got an allocation. It’s crucial that each one buyers perceive this, and we hope to put out the arguments for why, utilizing the credit score markets as the obvious class that should embrace the “cash of the web.”

However first, we must be on the same footing concerning our understanding of mounted earnings, and the assorted devices that exist within the market that permit for buyers to take danger, handle danger (hedge), earn returns and/or expertise losses.

Credit score is absolutely misunderstood by most small buyers. In reality, for my part, credit score can also be misunderstood by {many professional} buyers and asset allocators. As considered one of Canada’s first two sell-side excessive yield (HY) bond merchants (the esteemed David Gluskin of Goldman Sachs Canada being the opposite), I’ve lived many head-scratching moments on the buying and selling desks on Bay Avenue and Wall Avenue.

This abstract is pretty basic, and doesn’t dive into the subtleties of assorted mounted earnings constructions or investments. The aim is to get everybody on the same degree in order that we are able to suggest a framework that may assist future generations keep away from the errors of the previous. Certainly, those that don’t study from historical past are doomed to repeat it.

Our plan is to start out by explaining, in very basic and easy phrases, the credit score markets with explicit consideration to bonds and bond math. From there, we’ll dive into bond dangers and the everyday mechanics of a credit score disaster, and describe what is supposed by “contagion” (partly two of this sequence). We are going to then conclude by presenting a valuation mannequin for bitcoin when contemplating it as default insurance coverage on a basket of sovereigns/fiats (partly three of the sequence).

(Notice: This can be a deep topic. For additional studying, the Bible for mounted earnings investing is “The Handbook Of Fastened Revenue Securities” by Frank Fabozzi. This “handbook” is 1,400-plus pages of inexperienced eyeshade studying. It was required studying for my CFA, and it was often seen, in a number of editions and phases of disrepair, on each buying and selling desk the place I’ve labored).

Credit score Markets

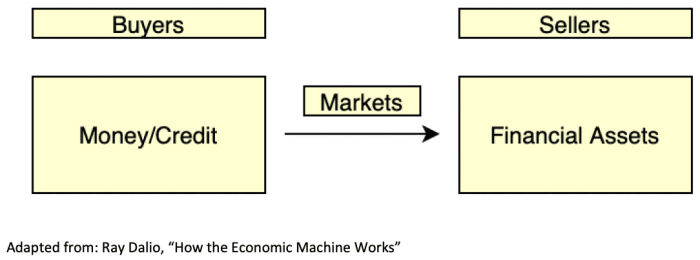

To grasp credit score (and credit score markets), one should first “zoom out” a bit to the broader monetary asset market, which from a excessive degree, could be illustrated as follows:

Illustrating the broader monetary market.

The three primary individuals on this market are governments, companies and particular person buyers. A glimpse on the breakdown of the U.S. fixed-income market demonstrates this:

| U.S. Fastened-Revenue Market (As Of June 30, 2021) | |

|---|---|

|

Sector |

Excellent Debt (Trillions) |

|

Governments |

$23.3 |

|

Retail Mortgage |

$11.7 |

|

Company |

$10.0 |

|

Different |

$2.5 |

So, why are monetary belongings purchased and offered within the first place? Patrons of monetary belongings (buyers) want to stretch the current into the longer term, and forego the speedy availability of cash/credit score within the hope of producing yield/return over time. Conversely, sellers of monetary belongings (companies, governments, and so on.) want to drag the longer term into the current, and entry liquid capital (cash) to serve present-day money circulation wants and develop future money circulation streams.

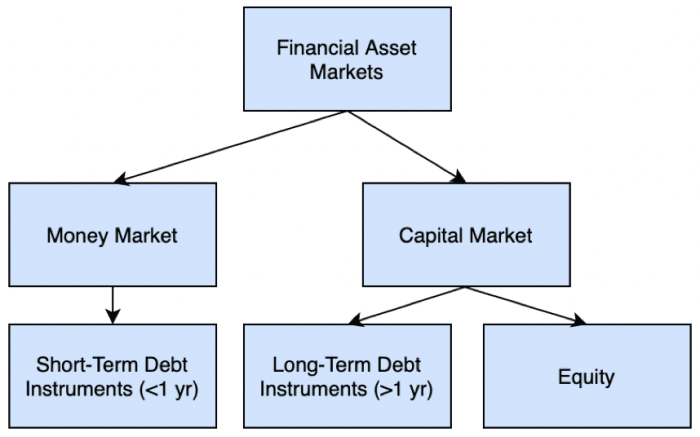

The next diagram highlights the “capital stack” (monetary belongings), which can be obtainable to patrons and sellers:

Capital stack obtainable to patrons and sellers

There are lots of devices inside these markets, all of which accomplish related objectives for each the issuer and the purchaser. These devices embody, however aren’t restricted to:

- Cash market devices, that are short-term debt agreements and embody federal funds, U.S. Treasury payments, certificates of deposit, repurchase (“repo”) and reverse repo agreements and industrial paper/asset-backed industrial paper.

- Capital market debt devices, that are long-term (multiple yr) debt agreements and embody: U.S. Treasury bonds, state/municipal bonds, “investment-grade” company bonds, “high-yield” company (“junk”) bonds and asset-backed securities (e.g., mortgage-backed securities).

- Fairness devices, which embody widespread and most well-liked inventory.

To place these markets into perspective, the scale of the worldwide credit score/debt market is roughly $400 trillion in keeping with Greg Foss and Jeff Sales space, as in comparison with the worldwide fairness market, which is a mere $100 trillion.

Inside this $400 trillion debt pool, the publicly-traded devices (bonds) have various phrases to maturity, starting from 30 days (treasury payments) as much as 100 years. The title “notes” is utilized to devices maturing in two-to-five years, whereas “bonds” confer with 10-year phrases, and “lengthy bonds” confer with bonds with maturities of higher than 20 years. It’s price noting that phrases of longer than 30 years aren’t widespread, though Austria has issued a 100-year bond. Good state treasurer. Why? As a result of, as shall be proven in subsequent sections, long-term funding at ultra-low charges locks in funding prices and strikes the chance burden to the customer.

Curiosity Charges And Yield Curves

Pulling the longer term into the current and producing liquidity is just not free. The client of the monetary asset expects a return on their capital. However what ought to this return be? 1%? 5%? 10%? Effectively, it relies on two primary variables: length and danger.

To simplify this, let’s take danger out of the equation and focus strictly on length. When doing so, one is ready to assemble a yield curve of U.S. treasuries as a perform of time. For instance, under is a chart taken from January 2021:

U.S. treasuries, January 2021

As you possibly can see, the yield curve right here is mostly “upward-sloping,” implying that devices of longer length carry the next yield. That is known as the “time period construction of rates of interest.”

We acknowledged that the above takes danger “out of the equation.” If we settle for the U.S. Treasury yield curve because the risk-free rate of interest, we are able to calculate the suitable price on all different debt devices from it. That is performed by making use of a “danger premium” above the risk-free price. Notice: that is additionally known as a “credit score unfold.”

Elements affecting the chance premium/credit score unfold embody:

Elements affecting danger premium and credit score unfold

‘Danger-Free’ Charges And Authorities Debtors

Earlier than diving deep into mounted earnings devices/bonds, let’s first revisit this idea of the “risk-free price” because it pertains to authorities/sovereign debtors…

Authorities bonds are probably the most extensively held mounted earnings instrument: Each insurance coverage firm, pension fund and most massive and small establishments personal them. Extra particularly, U.S. authorities bonds have usually been known as “risk-free” benchmarks, and thus the yield curve within the U.S. units the “risk-free price” for all given phrases.

The form of the yield curve is a topic of nice financial evaluation, and in an period when charges weren’t manipulated by central financial institution interference, the yield curve was helpful in predicting recessions, inflation and progress cycles. At present, in an period of QE and yield curve management, I consider the predictive energy of the yield curve is vastly diminished. It’s nonetheless an especially vital graph of presidency charges, and absolutely the value of borrowing, however there may be an elephant within the room… and that’s the assertion that certainly these charges are “risk-free.”

To the touch briefly on yield curve management (YCC)… Keep in mind the dialogue concerning the Fed supporting asset costs? YCC is when the Fed particularly helps treasury bond costs by not permitting the yield to extend above a sure threshold. Comply with alongside within the coming sections, however trace: as bond costs fall, bond yields rise.

Given the fact of the exorbitantly-high debt ranges up to date governments have accrued, I don’t consider you could possibly declare there may be no danger to the creditor. The dangers could also be low, however they aren’t zero. Regardless, we’ll get into the chance(s) inherent to mounted earnings devices (particularly bonds) in subsequent sections. However first, some fundamentals about bonds.

Fastened Revenue/Bond Fundamentals

Because the title implies, a fixed-income instrument is a contractual obligation that agrees to pay a stream of mounted funds from borrower to lender. There’s a cost obligation known as “the coupon” within the case of a bond contract, or “the unfold” within the case of a mortgage contract. There may be additionally a time period on the contract the place the principal quantity of the contract is totally repaid at maturity.

The coupon cost is outlined within the debt contract, and is often paid semi-annually.

Notably, not all bonds pay a coupon. Thus, there are two kinds of bonds:

- Zero-coupon/Low cost: Solely pay principal at maturity. The return for the investor merely includes “lending” an entity $98 to be paid $100 a yr later (for instance).

- Coupon-bearing: Pay periodic coupon and principal at maturity.

For now, you will need to notice that lending is an uneven (to the draw back) endeavor. If a borrower is doing nicely, the borrower doesn’t improve the coupon or mounted cost on the duty. That profit accrues to the fairness house owners. In reality, if the chance profile has modified for the higher, the borrower will doubtless pay down the duty and refinance at a decrease value, which once more advantages the fairness. The lender could be out of luck since their extra helpful contract is paid down, and they aren’t in a position to reap the engaging risk-adjusted returns.

To reiterate, the money flows on a bond contract are mounted. That is vital for a few causes. First, if the chance profile of the borrower adjustments, the cost stream doesn’t change to mirror the modified danger profile. In different phrases, if the borrower turns into extra dangerous (as a result of poor monetary efficiency) the funds are too low for the chance, and the worth/value of the contract will fall. Conversely, if the chance profile has improved, the cost stream remains to be mounted, and the worth of the contract will rise.

Lastly, discover that we’ve got but to precise our agreed upon unit of account in our “contract.” I think about everybody simply assumed the contract was priced in {dollars} or another fiat denomination. There is no such thing as a stipulation that the contract must be priced in fiat; nonetheless, virtually all mounted earnings contracts are. There are issues with this as shall be mentioned in future sections. In the interim, hold an open thoughts that the contracts may be priced in models of gold (ounces), models of bitcoin (satoshis), or in some other unit that’s divisible, verifiable and transferable.

The underside line is that this: The one variable that adjustments to mirror danger and market circumstances is the worth of the bond contract on the secondary market.

Credit score Vs. Fairness Markets

It’s my opinion that the credit score markets are extra ruthless than the fairness markets. If you’re proper, you’re paid a coupon and also you get your principal returned. If you’re mistaken, the curiosity coupon is in jeopardy (as a result of the opportunity of default), the worth of the credit score instrument begins to fall towards some type of restoration worth, and contagion comes into play. In brief, I rapidly discovered to play chances and use anticipated worth evaluation. In different phrases: You’ll be able to by no means be 100% sure of something.

Given this, credit score guys/bond buyers (“bondies”) are pessimists. In consequence, we are likely to ask “how a lot can I lose”? Fairness merchants and buyers, then again, are usually optimists. They consider bushes develop to the moon, and are usually greater danger takers than bondies, every part else being equal. This isn’t stunning since their precedence of declare ranks under that of credit score.

Within the occasion a company debt issuer is unable to make cost on a debt contract (default/chapter), there are “precedence of declare” guidelines. As such, secured debt holders have first proper of declare to any residual liquidation worth, unsecured debt holders are subsequent to obtain full or partial compensation of debt and fairness holders are the final (often receiving no residual worth). Of observe, it’s generally understood that typical restoration charges of excellent debt throughout a default are on the order of 35% to 40% of complete liabilities.

Moreover, if the widespread fairness pays a dividend, this isn’t a hard and fast earnings instrument as there isn’t any contract. The earnings belief market in Canada was constructed on this false premise. Fairness analysts would calculate the “dividend yield” on the fairness instrument and examine it to the yield to maturity (YTM) of a company bond and proclaim the relative worth of the instrument. Too many buyers in these earnings trusts have been fooled by this narrative, to not point out the businesses that have been utilizing helpful capital for dividend distributions as a substitute of progress capital expenditures (“cap ex”). For the love of our youngsters, we can’t let this kind of silly cash administration ideology to fester.

If you happen to handle cash professionally, equities are for capital beneficial properties, whereas bonds are for capital preservation. Fairness guys are anticipated to lose cash on many positions supplied their winners far outstrip the losers. Bondies have a tougher balancing act: Since all bonds are capped to the upside, however their worth could be minimize in half an infinite variety of occasions, you want many extra performing positions to offset people who underperform or default. As such, bondies are usually consultants in danger. Good fairness buyers take clues from the credit score markets. Sadly, it’s only some who ever do.

Bond Math 101

Each bond that trades within the secondary markets began its life as a brand new subject. It has a hard and fast contractual time period, semi-annual coupon cost and principal worth. Usually talking, new points are dropped at market with a coupon equal to its YTM. For example, a 4% YTM new subject bond is purchased at a value of par (100 cents on the greenback) with a contractual obligation to pay two semi-annual coupons of two% every.

After issuance, there’s a pretty liquid secondary market that develops for the bond. Future bond trades are impacted by provide and demand as a result of such issues as a change within the basic degree of rates of interest, a change within the precise or perceived credit score high quality of the issuer or a change in general market sentiment (danger urge for food adjustments impacting all bond costs and implied bond spreads). A bond value is set in an open market “over-the-counter” (OTC) transaction between a purchaser and a vendor.

The value of a bond is impacted by the YTM that’s implied within the transaction. If the “market required yield” has elevated as a result of credit score danger or inflation expectations, the implied rate of interest improve signifies that the worth of the bond will commerce decrease. If the bond was issued at par, then new trades will happen at a reduction to par. The other additionally applies.

For these of you who suppose the above makes good sense, be at liberty to skip this part. For the remainder of us, let’s stroll by bond math one step at a time.

We are able to worth every sort of bond, at issuance, within the following means:

Zero coupon/Low cost: The current worth of the longer term principal money circulation. The important thing element to this method, and that which is commonly missed by newcomers, is that the time period “r” describes exterior funding alternatives of equal danger. Thus:

The place:

- P = bond value as we speak

- A = principal paid at maturity

- r = market required yield (present rate of interest at which debt of equal danger is priced)

- t = variety of durations (should match interval of “r”) into the longer term the principal is to be repaid

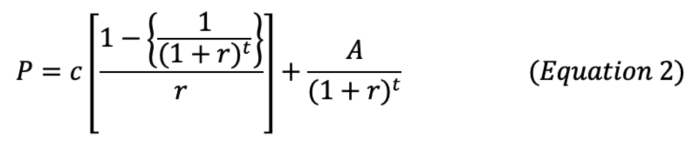

Coupon-bearing: The sum of the current worth of future money flows from each coupon funds and principal. Once more, the important thing element to this method, and that which is commonly missed by newcomers, is that the time period “r” describes exterior funding alternatives of equal danger. Thus:

The place:

- P = bond value as we speak

- c = coupon cost (in {dollars})

- A = principal paid at maturity

- r = market required yield (present rate of interest at which debt of equal danger is priced)

- t = variety of durations (should match interval of “r”) into the longer term the principal is to be repaid

Notice: If the contractual coupon price of a bond a is greater than the present charges provided by bonds of equal danger, the worth of bond a will increase (“premium bond”). Conversely, if the coupon price of bond a is decrease than bonds of equal danger, the worth of bond a decreases.

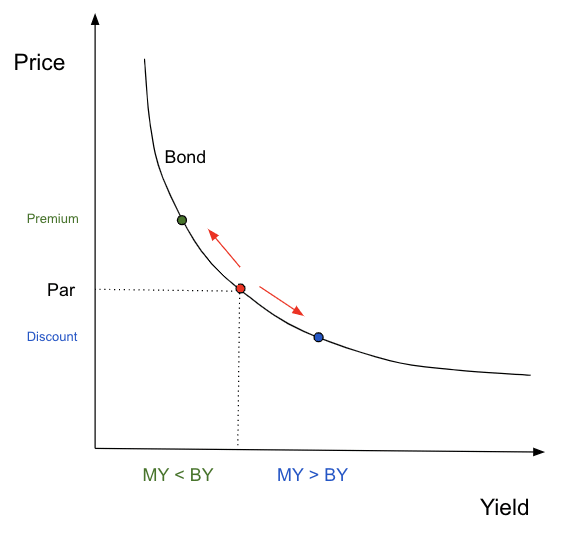

Stated in a different way, a bond’s value adjustments so that its yield matches the yield of an out of doors funding alternative of equal danger. This will also be illustrated as follows:

Notice: “MY” is market required yield, “BY” is yield of bond that investor is holding.

In contemplating the above equations and graph, the next truths turn into obvious:

- When a bond’s coupon price is the same as the market yield, the bond is priced at par.

- When a bond’s coupon price is lower than the market yield, the bond’s value is lower than par (low cost).

- When a bond’s coupon price is larger than the market yield, the bond’s value is larger than par (premium).

It is because bonds are a contract, promising to pay a hard and fast coupon. The one variable that may change is the worth of the contract as it’s traded on the secondary market. Whereas we now perceive how the prevailing rate of interest out there impacts bond costs, you will need to observe that this isn’t the one issue that may have an effect on these costs. As we explored earlier, yields/rates of interest mirror danger, and there may be certainly multiple danger associated to investing in a bond. We are going to discover these dangers extra partly two of this sequence.

Bond Math 201

Calculating a change in bond value as a perform of the change in “market required yield” utilizing sensitivity evaluation makes use of its first by-product (length) and its second by-product (convexity) to find out a value change. For a given change in rate of interest, the worth change within the bond is calculated as adverse length occasions the change in rate of interest plus one half of the convexity occasions the change in rate of interest squared. If readers bear in mind their physics formulation for distance, the change in value is just like the change in distance, length is like the speed and convexity is like acceleration. It’s a Taylor sequence. Math could be cool.

Math might, in truth, be cool, nevertheless it certain as hell isn’t enjoyable generally. A few issues to recollect earlier than we get deep into the arithmetic:

- When the market required yield adjustments, the % change in bond pricing is just not the identical for all bonds. That’s, the next elements trigger higher value sensitivity to a given change in market required yield: Longer maturity and decrease coupon price.

- The value improve of bonds (when market yields fall) is larger than the worth lower of bonds (when market yields rise).

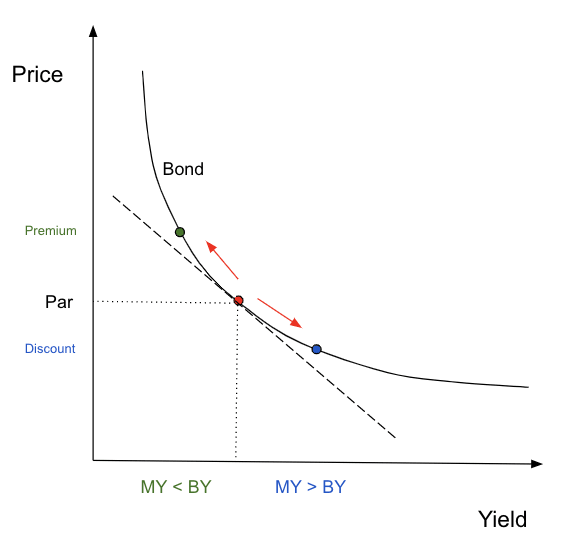

Period: The First By-product

So, then, what’s the % value change in a given bond for a given change in market-required yield? That is what length provides us… strictly outlined, length is the approximate share change in a bond’s value for each 1% (100 foundation factors [bps]) change in market required yield. Mathematically, that is expressed as:

The place:

- V- is value of bond if market required yield decreases x bps

- V+ is value of bond if market required yield will increase z bps

- Vo is value of bond at present market yield

- ▵y is z bps (expressed as decimal)

Just a few issues to pay attention to:

- V- and V+ are derived from equation two

- The above equation will present a quantity, and the unit of measure is in years. This doesn’t immediately reference time, reasonably it means “x bond has a value sensitivity to price adjustments which is similar as a ___ yr zero coupon bond.”

From the above equation, the approximate share change in bond value (A) for any given change in charges could be calculated as follows:

The place:

- ▵y is the change in market required yield, in bps (expressed as decimal)

This relationship could be utilized to any change in foundation factors as a result of the length equation is a linear perform. Keep in mind the worth/yield curve from earlier? Right here it’s once more, with the addition of length (dashed line).

Discover two issues: length approximates the change in bond value way more precisely if the change in yield is small, and length calculations will all the time underestimate value. Given the truth that length is linear, whereas the worth/yield curve is convex in form, this ought to be evident.

So, since length is just not fully correct, how can we enhance upon it?

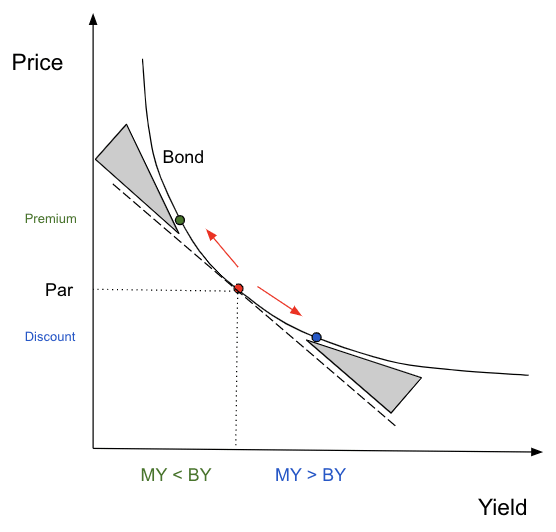

Convexity: The Second By-product

It’s really solely a coincidence that the second by-product is termed convexity, whereas the shortcoming of the length calculation is that it fails to account for the convexity of the worth/yield curve. Regardless, it’s helpful to assist us bear in mind the idea…

In different phrases, convexity helps to measure the change in bond value as a perform of the change in yield that isn’t defined by length.

An image right here is useful:

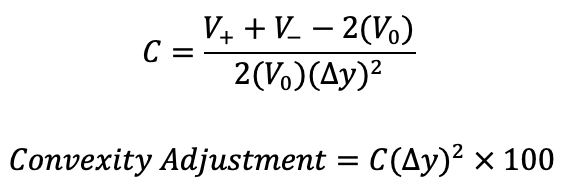

Convexity, as is proven, “adjusts” the length estimate by the quantity within the shaded grey space. This “convexity measure,” C, could be calculated as follows:

Armed with this data, you at the moment are in a position to calculate the approximate value change of a bond as a perform of the adjustments in market required yield/rates of interest. I’d emphasize that performing the precise calculations isn’t mandatory, however understanding the ideas is. For instance, it ought to now make sense that for a 100 bps improve in market yield, the worth of long-dated (30-year) bonds will drop roughly 20%. All that mentioned, I’m nonetheless undecided what a Taylor sequence is (so don’t ask).

Conclusion

You now (hopefully) have a greater understanding of the credit score markets, bonds and bond math. Within the subsequent installment (half two), we’ll construct on this data by diving into bond dangers and contagion.

In closing, we emphatically reiterate: Select your retailer of worth properly. By no means cease studying. The world is dynamic.

This can be a visitor submit by Greg Foss and Jason Sansone. Opinions expressed are fully their very own and don’t essentially mirror these of BTC Inc or Bitcoin Journal.